# Here are the libraries I used

library(tidyverse) # standard

library(knitr) # need for a couple things to make knitted document to look nice

library(readr) # need to read in data

library(ggpubr) # allows for stat_cor in ggplots

library(ggfortify) # Needed for autoplot to work on lm()

library(gridExtra) # allows me to organize the graphs in a grid

library(car) # need for some regression stuff like vif

library(GGally)

library(Hmisc) # Needed for some visuals

library(rms) # needed for some data reduction tech.

library(pcaPP)

library(see)

library(performance)9 Variable Selection, Data Reduction, and Model Comparison

Here are some code chunks that setup this document.

# This changes the default theme of ggplot

old.theme <- theme_get()

theme_set(theme_bw())9.1 Explainable statistical learning in public health for policy development: the case of real-world suicide data

We will work with data made available from this paper:

https://bmcmedresmethodol.biomedcentral.com/articles/10.1186/s12874-019-0796-7

If you want to go really in-depth of how you deal with data, this article goes into a lot of detail.

phe <- read_csv(here::here("datasets","phe.csv"))9.1.1 Variables. A LOT!

| Variables |

|---|

| 2014 Suicide (age-standardised rate per 100,000 - outcome measure) |

| 2013 Adult social care users who have as much social contact as they would like (% of adult social care users) |

| 2013 Adults in treatment at specialist alcohol misuse services (rate per 1000 population) |

| 2013 Adults in treatment at specialist drug misuse services (rate per 1000 population) |

| 2013 Alcohol-related hospital admission (female) (directly standardised rate per 100,000 female population) |

| 2013 Alcohol-related hospital admission (male) (directly standardised rate per 100,000 male population) |

| 2013 Alcohol-related hospital admission (directly standardised rate per 100,000 population) |

| 2013 Children in the youth justice system (rate per 1,000 aged 10–18) |

| 2013 Children leaving care (rate per 10,000 < 18 population) |

| 2013 Depression recorded prevalence (% of adults with a new diagnosis of depression who had a bio-psychosocial assessment) |

| 2013 Domestic abuse incidents (rate per 1,000 population) |

| 2013 Emergency hospital admissions for intentional self-harm (female) (directly age-standardised rate per 100,000 women) |

| 2013 Emergency hospital admissions for intentional self-harm (male) (directly age-standardised rate per 100,000 men) |

| 2013 Emergency hospital admissions for intentional self-harm (directly age-and-sex-standardised rate per 100,000) |

| 2013 Looked after children (rate per 10,000 < 18 population) |

| 2013 Self-reported well-being - high anxiety (% of people) |

| 2013 Severe mental illness recorded prevalence (% of practice register [all ages]) |

| 2013 Social care mental health clients receiving services (rate per 100,000 population) |

| 2013 Statutory homelessness (rate per 1000 households) |

| 2013 Successful completion of alcohol treatment (% who do not represent within 6 months) |

| 2013 Successful completion of drug treatment - non-opiate users (% who do not represent within 6 months) |

| 2013 Successful completion of drug treatment - opiate users (% who do not represent within 6 months) |

| 2013 Unemployment (% of working-age population) |

| 2012 Adult carers who have as much social contact as they would like (18+ yrs) (% of 18+ carers) |

| 2012 Adult carers who have as much social contact as they would like (all ages) (% of adult carers) |

| 2011 Estimated prevalence of opiates and/or crack cocaine use (rate per 1,000 aged 15–64) |

| 2011 Long-term health problems or disability (% of people whose day-to-day activities are limited by their health or disability) |

| 2011 Marital breakup (% of adults whose current marital status is separated or divorced) |

| 2011 Older people living alone (% of households occupied by a single person aged 65 or over) |

| 2011 People living alone (% of all households occupied by a single person) |

| Mental Health Service users with crisis plans: % of people in contact with services with a crisis plan in place (end of quarter snapshot) |

| Older people |

| 2011 Self-reported well-being - low happiness (% of people with a low happiness score) |

9.2 How do we choose variables?

Objective: Find a way to predict suicide rates.

We could just use all of the predictors in a linear model.

fullLm <- lm(suicide_rate ~ ., phe)

summary(fullLm)

Call:

lm(formula = suicide_rate ~ ., data = phe)

Residuals:

Min 1Q Median 3Q Max

-3.0118 -1.0447 -0.2702 0.9903 4.1993

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 2.0155877 3.5059381 0.575 0.566

children_youth_justice -0.0235629 0.0247292 -0.953 0.343

adult_carers_isolated_18 0.0336685 0.0262501 1.283 0.202

adult_carers_isolated_all_ages -0.0226404 0.0424220 -0.534 0.595

adult_carers_not_isolated 0.3786174 0.2379446 1.591 0.114

alcohol_rx_18 -0.3001189 0.2515821 -1.193 0.235

alcohol_rx_all_ages -0.0130574 0.0148093 -0.882 0.380

alcohol_admissions_f -0.0060296 0.0127911 -0.471 0.638

alchol_admissions_m 0.0167345 0.0268020 0.624 0.534

alcohol_admissions_p -0.0600782 0.0895445 -0.671 0.504

children_leaving_care 0.0216349 0.0288644 0.750 0.455

depression -0.1169805 0.1328876 -0.880 0.380

domestic_abuse 0.0269278 0.0419236 0.642 0.522

self_harm_female 0.0369915 0.0946913 0.391 0.697

self_harm_male 0.0318458 0.0944774 0.337 0.737

self_harm_persons -0.0658812 0.1902674 -0.346 0.730

opiates 0.2041520 0.1375203 1.485 0.140

lt_health_problems 0.0318830 0.1456081 0.219 0.827

lt_unepmloyment -0.6342130 1.2588572 -0.504 0.615

looked_after_children 0.0174365 0.0146237 1.192 0.236

marital_breakup 0.1606036 0.1723378 0.932 0.353

old_pople_alone 0.3779967 0.4371635 0.865 0.389

alone -0.1004305 0.1386281 -0.724 0.470

self_reported_well_being 0.0605038 0.0681410 0.888 0.376

smi 2.1708482 1.3401643 1.620 0.108

social_care_mh 0.0006815 0.0005270 1.293 0.199

homeless -0.1550536 0.1051424 -1.475 0.143

alcohol_rx 0.0170587 0.0282631 0.604 0.547

drug_rx_non_opiate -0.0408008 0.0271119 -1.505 0.135

drug_rx_opiate 0.1068925 0.0848400 1.260 0.210

unemployment 0.0690206 0.2925910 0.236 0.814

Residual standard error: 1.687 on 118 degrees of freedom

Multiple R-squared: 0.5031, Adjusted R-squared: 0.3767

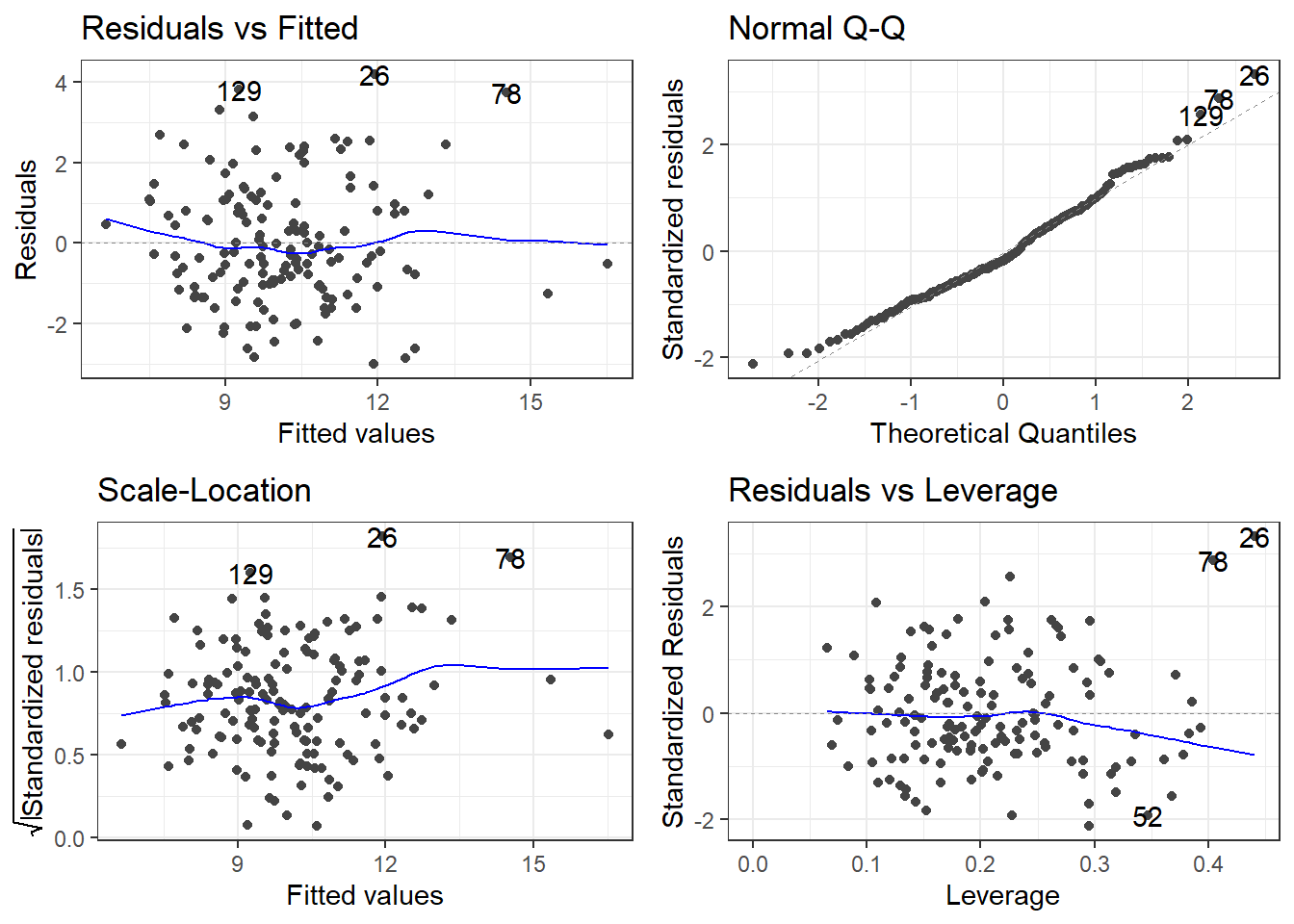

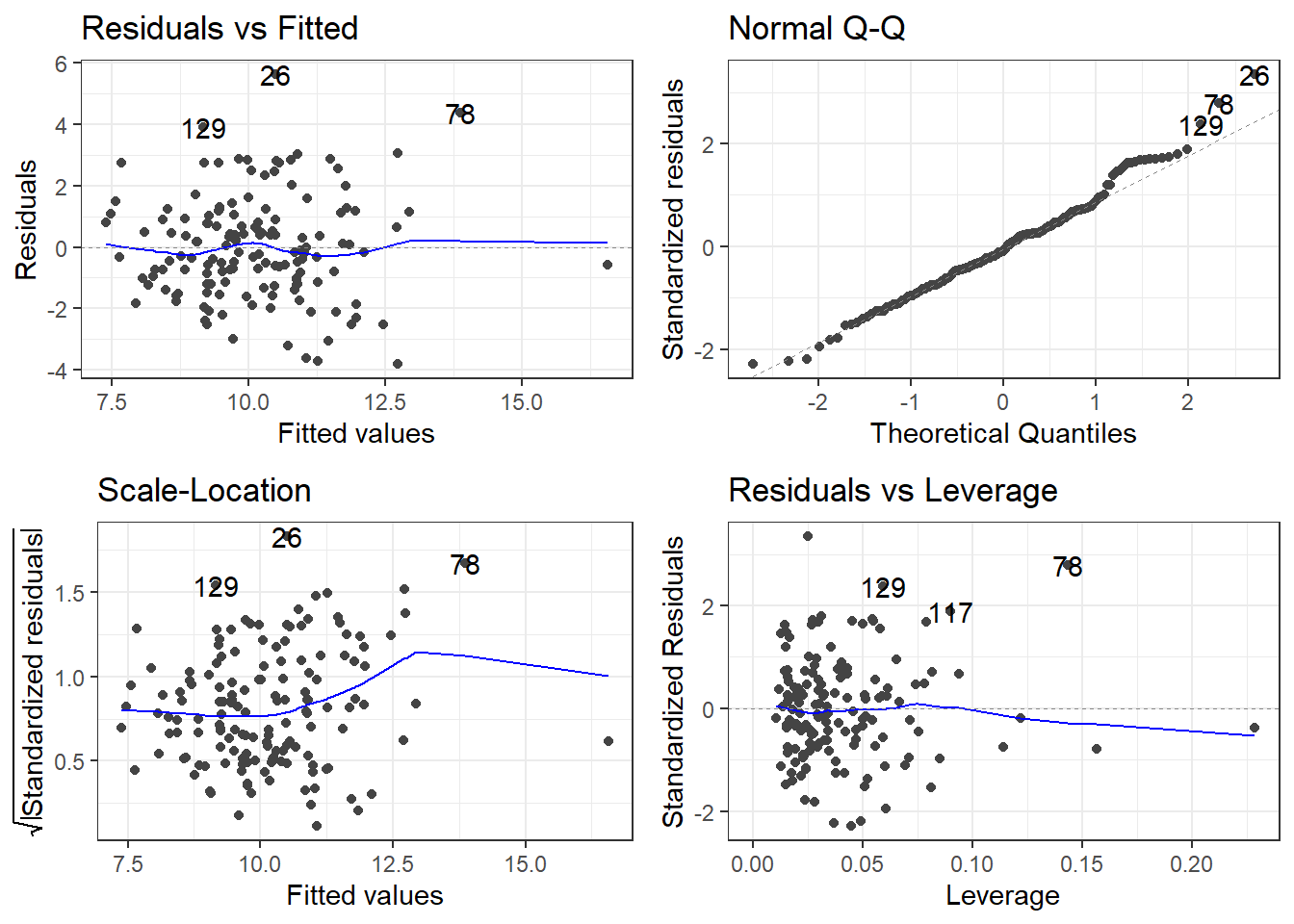

F-statistic: 3.982 on 30 and 118 DF, p-value: 3.823e-08autoplot(fullLm)

If we are going by statistical significance, each predictor variable fails but the global F-test says that a linear model is working (sort of).

And that \(R^2\) is pretty good for “prediciting” something related to human behavior.

Residuals look good.

Overall, this is bad!

You do not just use all the variables you have

Though there are exceptions: read Harrell’s Regression Model Strategies (Chapter 4, Section 12, 4.12.1 - 4.12.3)

9.2.1 The scope of the problem

How many variables are there to use…? How well do they work?

We could try cor(phe) and see which variables are most correlated with suicide_rate. (You’ll get a lot of output… that’s \(31\times 31 = 961\) correlations)

I’ll save you the pain and just show the correlations with just suicide_rate.

suicide_rate

children_youth_justice 0.05847330

adult_carers_isolated_18 0.24939518

adult_carers_isolated_all_ages 0.20369843

adult_carers_not_isolated 0.45228878

alcohol_rx_18 0.38997284

alcohol_rx_all_ages 0.33117982

alcohol_admissions_f 0.29906808

alchol_admissions_m 0.31868168

alcohol_admissions_p 0.11433511

children_leaving_care 0.36700280

depression 0.32509700

domestic_abuse 0.14835220

self_harm_female 0.49025136

self_harm_male 0.52004798

self_harm_persons 0.51686092

opiates 0.41195709

lt_health_problems 0.47825399

lt_unepmloyment 0.19643927

looked_after_children 0.51243274

marital_breakup 0.39971208

old_pople_alone 0.39870200

alone 0.31037882

self_reported_well_being 0.12949288

smi 0.18390513

social_care_mh 0.20125278

homeless -0.32105739

alcohol_rx -0.07513134

drug_rx_non_opiate -0.14207504

drug_rx_opiate -0.14345307

unemployment 0.188271389.2.2 Just use the best correlations?

These are a few of the strongest correlations.

suicide_rate

self_harm_female 0.49025136

self_harm_male 0.52004798

self_harm_persons 0.51686092

looked_after_children 0.51243274Let’s make a model.

badIdea <- lm(suicide_rate ~ self_harm_female + self_harm_male + self_harm_persons + looked_after_children, phe)

summary(badIdea)

Call:

lm(formula = suicide_rate ~ self_harm_female + self_harm_male +

self_harm_persons + looked_after_children, data = phe)

Residuals:

Min 1Q Median 3Q Max

-4.1974 -1.2196 0.0677 1.1319 6.4354

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 6.521275 0.485989 13.419 < 2e-16 ***

self_harm_female 0.059297 0.087465 0.678 0.498889

self_harm_male 0.053601 0.087682 0.611 0.541954

self_harm_persons -0.106747 0.175961 -0.607 0.545038

looked_after_children 0.031342 0.008442 3.713 0.000292 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 1.763 on 144 degrees of freedom

Multiple R-squared: 0.3379, Adjusted R-squared: 0.3195

F-statistic: 18.37 on 4 and 144 DF, p-value: 3.246e-12What does the model have to say about how the self harm variables are related to suicide rate?

9.3 Multicollinearity

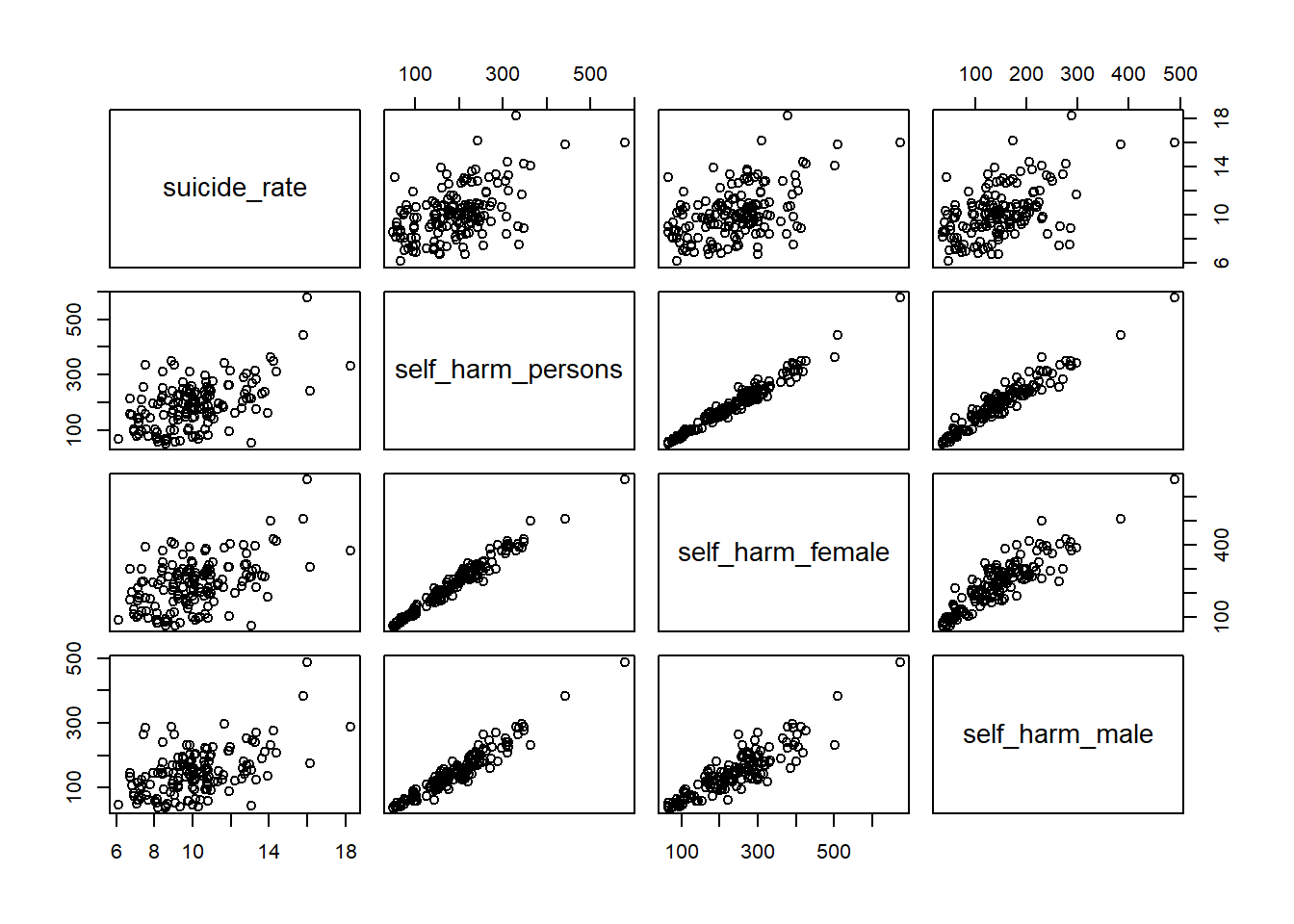

pairs(suicide_rate ~ self_harm_persons + self_harm_female + self_harm_male, phe)

cor(phe$self_harm_female,phe$self_harm_male)[1] 0.8865727cor(phe$self_harm_persons,phe$self_harm_male)[1] 0.9601094cor(phe$self_harm_persons,phe$self_harm_female)[1] 0.9804772When we have predictor variables that are linearly related to each other, we have what is called multi-collinearity.

These variables essentially all contribute the same information over and over to the model. This makes a feedback loop that kicks everything around.

What about a model with just self_harm_persons (Why that one?) and looked_after_children?

notAsBadLm <- lm(suicide_rate ~ self_harm_persons + looked_after_children, phe)

summary(notAsBadLm)

Call:

lm(formula = suicide_rate ~ self_harm_persons + looked_after_children,

data = phe)

Residuals:

Min 1Q Median 3Q Max

-4.3450 -1.2323 0.0677 1.0792 6.2763

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 6.704515 0.430054 15.590 < 2e-16 ***

self_harm_persons 0.008385 0.002124 3.947 0.000123 ***

looked_after_children 0.027803 0.007281 3.818 0.000198 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 1.756 on 146 degrees of freedom

Multiple R-squared: 0.3337, Adjusted R-squared: 0.3246

F-statistic: 36.56 on 2 and 146 DF, p-value: 1.344e-139.3.1 But what about self harm and looking after children?

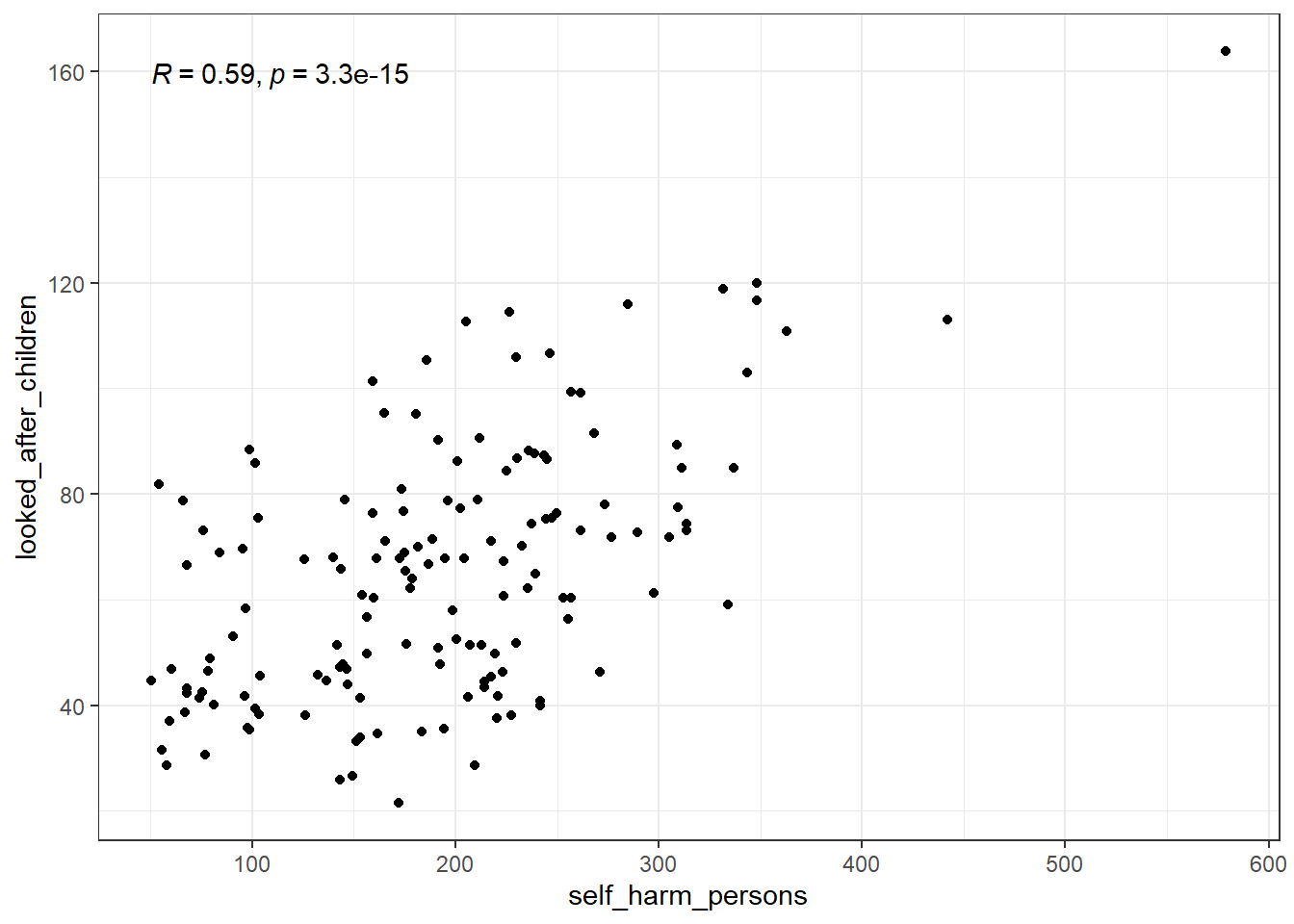

Relations may not be as blaringly obvious as that. What about self harm and looking after children?

ggplot(phe, aes(x = self_harm_persons, y = looked_after_children)) +

geom_point() +

stat_cor()

This isn’t nearly as bad and wouldn’t be considered a detrimental relation.

9.4 Measuring multi-collinearity

9.4.1 A linear model for the predictors

Linear relation between many predictor variables.

\[x_k =\beta_{0}^* + \beta_{1}^* x_1 + \beta_{2}^*x_2 + \dots + \beta_p^* x_p + \epsilon^*\]

This is like any model and has it’s own \(R^2\) \(R^2_k\).

If this \(R^2\) is high, it means that a predictor variable is redundant.

There are a few ways to measure “high”.

Some sources would say that \(0.8 \le R_k^2 \le 0.9\) would be problematic, and you have extreme multicollinearity issues for anything higher.

9.4.2 Tolerance

Tolerance is \(1 - R^2_k\).

That’s it.

So \(0.2\) is the “problematic” cutoff and \(0.9\) is the “extreme” cutoff.

It may be referred to as TOL sometimes.

9.4.3 Variance Inflation Factors

The Variance Inflation Factor is:

\[VIF_k = \frac{1}{1 - R^2_k}\]

The VIF is considered “problematic” if greater than 5, and “extreme” if greater than 10.

9.4.4 Getting TOL or VIF: performance package

A nifty package that will help us deal with all the nasty bits of linear regression in R is the performance package. It is part of the easystats universe of packages.

To get tolerance and VIFs, create the model using lm(), and then plug it into the check_collinearity function.

check_collinearity(model)

library(performance)

library(see)

# badidea was the model with all the self harm variables

check_collinearity(badIdea)# Check for Multicollinearity

Low Correlation

Term VIF VIF 95% CI Increased SE Tolerance

looked_after_children 2.04 [ 1.66, 2.63] 1.43 0.49

Tolerance 95% CI

[0.38, 0.60]

High Correlation

Term VIF VIF 95% CI Increased SE Tolerance

self_harm_female 3811.50 [2809.27, 5171.42] 61.74 2.62e-04

self_harm_male 1863.65 [1373.68, 2528.51] 43.17 5.37e-04

self_harm_persons 10400.43 [7665.39, 14111.48] 101.98 9.61e-05

Tolerance 95% CI

[0.00, 0.00]

[0.00, 0.00]

[0.00, 0.00]Versus

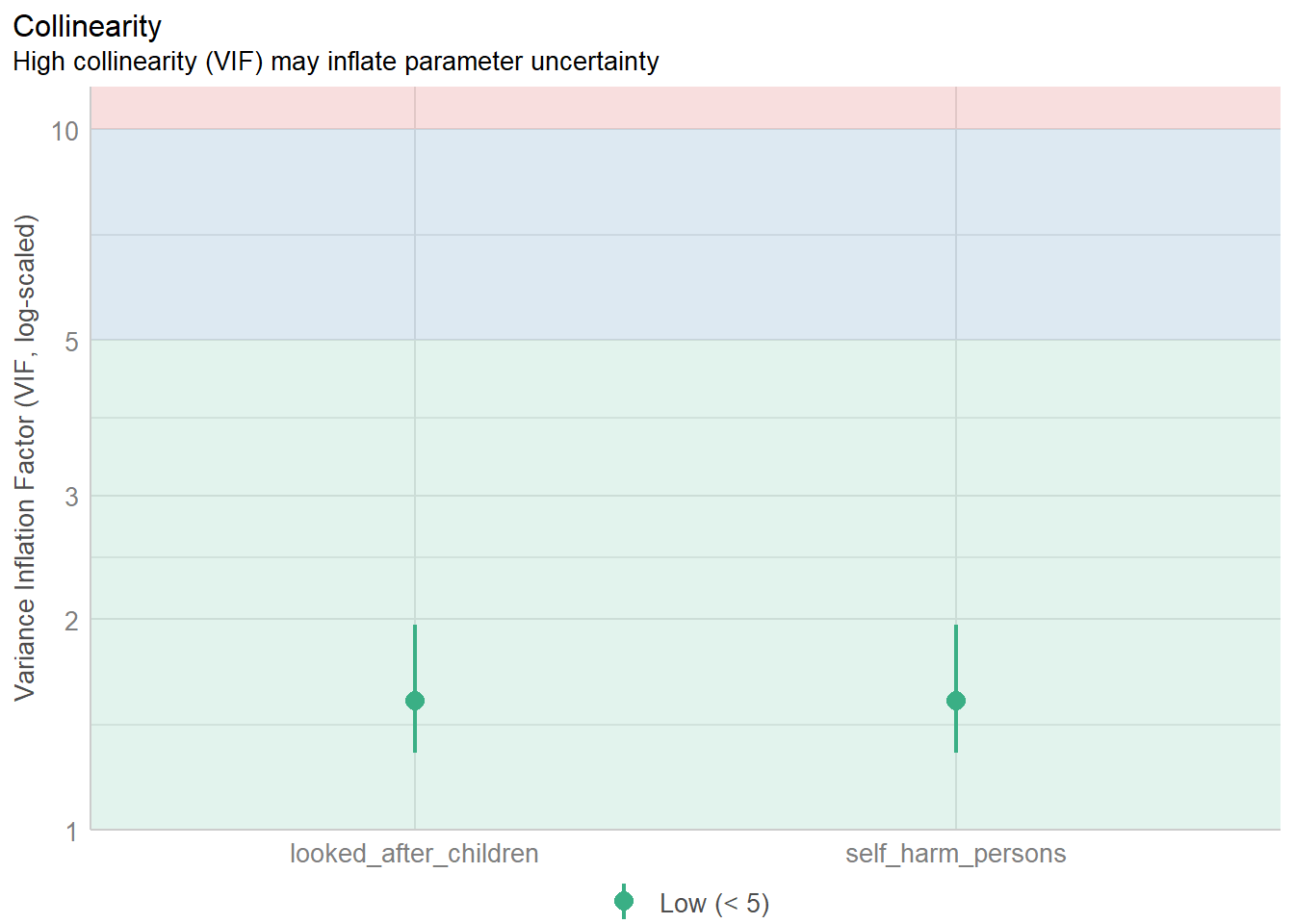

check_collinearity(notAsBadLm)# Check for Multicollinearity

Low Correlation

Term VIF VIF 95% CI Increased SE Tolerance

self_harm_persons 1.53 [1.29, 1.96] 1.24 0.65

looked_after_children 1.53 [1.29, 1.96] 1.24 0.65

Tolerance 95% CI

[0.51, 0.78]

[0.51, 0.78]9.4.5 Plot check_collinearity checks

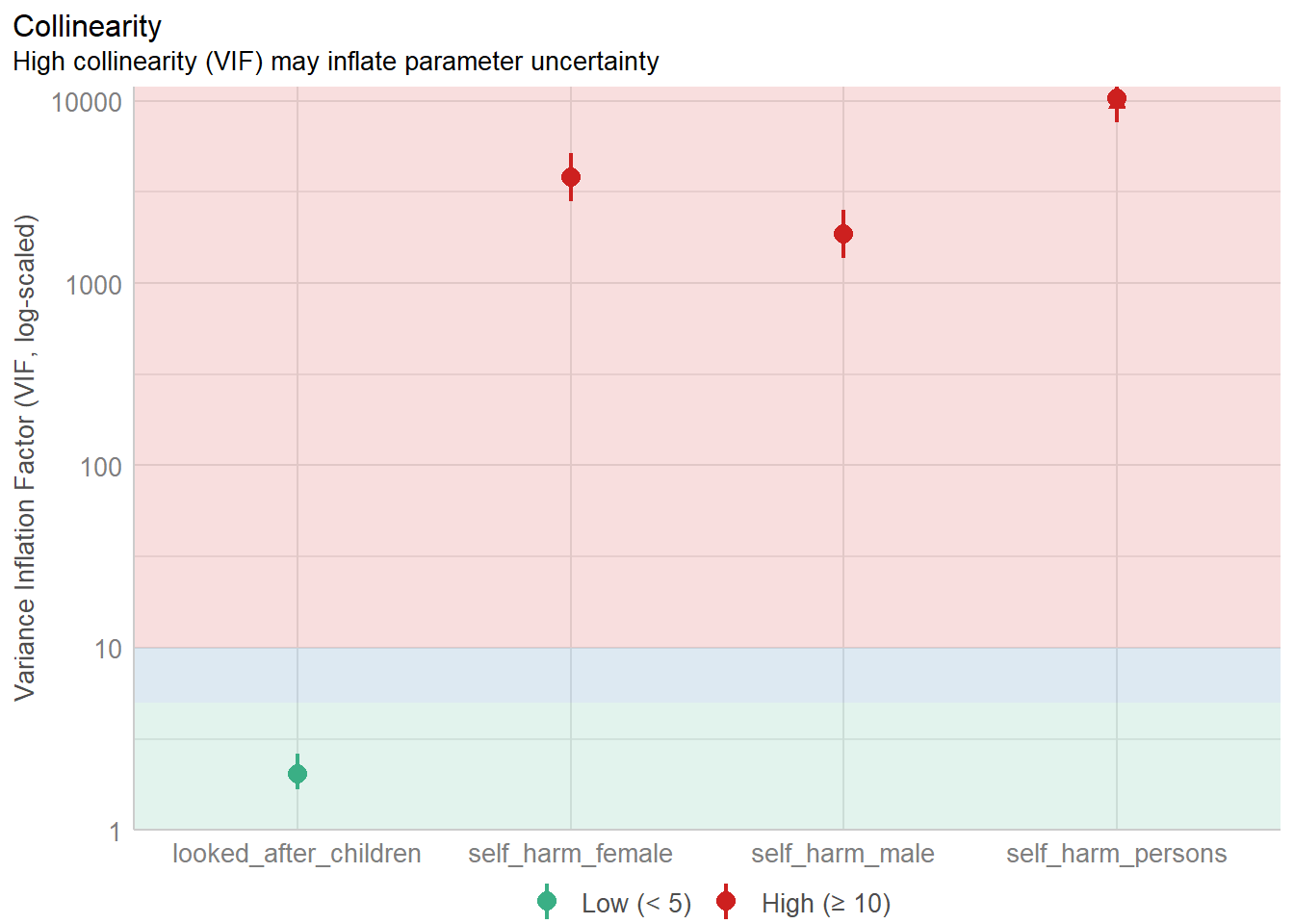

plot(check_collinearity(badIdea))

Versus

plot(check_collinearity(notAsBadLm))

9.4.6 VIF and Tolerance in the full model

You do not get rid of a variable because it has a small tolerance/large VIF!

You would investigate which variables are most correlated with eachother.

You need to use your own reasoning to decide which variables to remove based on the correlations between predictors AND the response.

Tolerance and VIF only indicate that the overall model has a problem, not the individual variable.

check_collinearity(fullLm)# Check for Multicollinearity

Low Correlation

Term VIF VIF 95% CI Increased SE

children_youth_justice 1.48 [ 1.29, 1.80] 1.22

adult_carers_isolated_18 1.88 [ 1.59, 2.30] 1.37

adult_carers_isolated_all_ages 1.84 [ 1.57, 2.26] 1.36

adult_carers_not_isolated 3.11 [ 2.55, 3.88] 1.76

alcohol_admissions_p 2.05 [ 1.73, 2.52] 1.43

children_leaving_care 4.32 [ 3.49, 5.42] 2.08

depression 2.73 [ 2.25, 3.38] 1.65

domestic_abuse 1.90 [ 1.61, 2.33] 1.38

marital_breakup 2.36 [ 1.97, 2.91] 1.54

alone 4.82 [ 3.88, 6.06] 2.19

self_reported_well_being 1.42 [ 1.24, 1.72] 1.19

smi 3.62 [ 2.94, 4.52] 1.90

social_care_mh 1.29 [ 1.15, 1.58] 1.14

homeless 3.11 [ 2.55, 3.87] 1.76

alcohol_rx 3.27 [ 2.68, 4.08] 1.81

drug_rx_non_opiate 3.21 [ 2.63, 4.00] 1.79

drug_rx_opiate 1.99 [ 1.68, 2.44] 1.41

Tolerance Tolerance 95% CI

0.68 [0.56, 0.78]

0.53 [0.43, 0.63]

0.54 [0.44, 0.64]

0.32 [0.26, 0.39]

0.49 [0.40, 0.58]

0.23 [0.18, 0.29]

0.37 [0.30, 0.44]

0.53 [0.43, 0.62]

0.42 [0.34, 0.51]

0.21 [0.16, 0.26]

0.71 [0.58, 0.81]

0.28 [0.22, 0.34]

0.77 [0.63, 0.87]

0.32 [0.26, 0.39]

0.31 [0.24, 0.37]

0.31 [0.25, 0.38]

0.50 [0.41, 0.60]

Moderate Correlation

Term VIF VIF 95% CI Increased SE Tolerance

lt_unepmloyment 5.30 [ 4.26, 6.68] 2.30 0.19

looked_after_children 6.68 [ 5.33, 8.45] 2.58 0.15

unemployment 8.68 [ 6.89, 11.02] 2.95 0.12

Tolerance 95% CI

[0.15, 0.23]

[0.12, 0.19]

[0.09, 0.15]

High Correlation

Term VIF VIF 95% CI Increased SE Tolerance

alcohol_rx_18 18.48 [ 14.52, 23.59] 4.30 0.05

alcohol_rx_all_ages 351.34 [ 273.84, 450.86] 18.74 2.85e-03

alcohol_admissions_f 978.20 [ 762.20, 1255.50] 31.28 1.02e-03

alchol_admissions_m 2345.59 [ 1827.47, 3010.68] 48.43 4.26e-04

self_harm_female 4877.78 [ 3800.20, 6261.00] 69.84 2.05e-04

self_harm_male 2362.51 [ 1840.66, 3032.40] 48.61 4.23e-04

self_harm_persons 13277.66 [10344.20, 17043.10] 115.23 7.53e-05

opiates 12.46 [ 9.83, 15.87] 3.53 0.08

lt_health_problems 11.71 [ 9.25, 14.91] 3.42 0.09

old_pople_alone 11.18 [ 8.84, 14.23] 3.34 0.09

Tolerance 95% CI

[0.04, 0.07]

[0.00, 0.00]

[0.00, 0.00]

[0.00, 0.00]

[0.00, 0.00]

[0.00, 0.00]

[0.00, 0.00]

[0.06, 0.10]

[0.07, 0.11]

[0.07, 0.11]You have to jump through a lot of hoops and then make justifiable choices.

9.4.7 Detecting Multicollinearity

The following our indicators of multicollinearity:

- “Significant” correlations between pairs of independent variables.

- Non-significant t-tests for all or nearly all of the predictor variables, but a significant global F-test.

- The coefficients have opposite signs than what would be expected (by logic or compared to the individual correlation with the response variable).

- A single VIF of 10, more than one VIF of 5 or above. Several VIF 3 or over. Or corresponding tolerance values. Or corresponding \(R^2_k\) values

The cutoffs for VIF, tolerance, or \(R^2_k\) are guidelines not solid rules. Theory should always trump these more arbitrary statistical rules.

9.5 Variable screening the PHE data

The paper has various methods for variable selection to remove multicollinearity issues.

They don’t really document it that well… Here’s my best take.

# I created this dataset after going through things over and over

# I removed variables from the csv as I was working with it in R

# Lots of fun!

# also, I only use this dataset for demonstration so I don't have to type out

# all of the variables I left in the data into the formula.

pheRed <- read_csv(here::here("datasets",

'phe_reduced.csv'))

redModel <- lm(suicide_rate ~ ., pheRed)

check_collinearity(redModel)# Check for Multicollinearity

Low Correlation

Term VIF VIF 95% CI Increased SE Tolerance

children_youth_justice 1.13 [1.04, 1.51] 1.06 0.88

adult_carers_isolated_all_ages 1.48 [1.27, 1.85] 1.22 0.68

alcohol_admissions_p 1.78 [1.49, 2.23] 1.33 0.56

children_leaving_care 2.58 [2.09, 3.30] 1.61 0.39

depression 2.21 [1.81, 2.80] 1.49 0.45

domestic_abuse 1.42 [1.23, 1.78] 1.19 0.70

self_harm_persons 2.35 [1.92, 2.99] 1.53 0.43

opiates 2.14 [1.76, 2.70] 1.46 0.47

marital_breakup 1.83 [1.53, 2.30] 1.35 0.55

alone 1.49 [1.28, 1.87] 1.22 0.67

self_reported_well_being 1.24 [1.10, 1.57] 1.11 0.81

social_care_mh 1.17 [1.05, 1.51] 1.08 0.86

homeless 2.25 [1.84, 2.86] 1.50 0.44

alcohol_rx 1.43 [1.24, 1.80] 1.20 0.70

drug_rx_opiate 1.62 [1.37, 2.03] 1.27 0.62

Tolerance 95% CI

[0.66, 0.97]

[0.54, 0.79]

[0.45, 0.67]

[0.30, 0.48]

[0.36, 0.55]

[0.56, 0.81]

[0.33, 0.52]

[0.37, 0.57]

[0.43, 0.65]

[0.54, 0.78]

[0.64, 0.91]

[0.66, 0.95]

[0.35, 0.54]

[0.56, 0.81]

[0.49, 0.73]Some variables I removed because I could not find the correct definition.

I am not an expert on this stuff so I had to do my best based on my mediocre knowledge of the subject matter, and trying to figure out what the authors of the paper were saying.

When it is okay to stop removing variables is entirely dependent on the situation. I don’t even have a guideline for it.

9.6 Next step: Choosing an actual model

Supposing the multicollinearity issue has been solved, how do we move on?

Do we use all the variables in the model?

summary(redModel)

Call:

lm(formula = suicide_rate ~ ., data = pheRed)

Residuals:

Min 1Q Median 3Q Max

-3.8689 -1.1154 -0.0917 0.8901 4.2030

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 4.0832859 3.0285950 1.348 0.1799

children_youth_justice -0.0136101 0.0220822 -0.616 0.5387

adult_carers_isolated_all_ages 0.0000509 0.0387482 0.001 0.9990

alcohol_admissions_p -0.0623441 0.0849678 -0.734 0.4644

children_leaving_care 0.0422261 0.0227752 1.854 0.0659 .

depression -0.1622739 0.1220073 -1.330 0.1858

domestic_abuse 0.0247253 0.0369822 0.669 0.5049

self_harm_persons 0.0066734 0.0025813 2.585 0.0108 *

opiates 0.1010386 0.0580642 1.740 0.0842 .

marital_breakup 0.2937180 0.1548091 1.897 0.0600 .

alone 0.0336382 0.0786620 0.428 0.6696

self_reported_well_being 0.0345748 0.0650050 0.532 0.5957

social_care_mh 0.0007603 0.0005101 1.490 0.1385

homeless -0.2377671 0.0912485 -2.606 0.0102 *

alcohol_rx -0.0047326 0.0190770 -0.248 0.8045

drug_rx_opiate 0.0305590 0.0779842 0.392 0.6958

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 1.72 on 133 degrees of freedom

Multiple R-squared: 0.4176, Adjusted R-squared: 0.3519

F-statistic: 6.358 on 15 and 133 DF, p-value: 5.163e-10Well now at least some of the predictor’s are significant.

We should not just use all predictors since that ruins the generalizibility of the model.

9.6.0.1 The principle of parsimony: Models should have as few variables/parameters as possible while retaining adequacy.

9.7 Methods for model assessment

We have many variables to choose from, and it’s really easy to make a model.

Should we just pick the variables most highly correlated with suicide rate?

What is our cutoff then?

suicide_rate

children_youth_justice 0.05847330

adult_carers_isolated_all_ages 0.20369843

alcohol_admissions_p 0.11433511

children_leaving_care 0.36700280

depression 0.32509700

domestic_abuse 0.14835220

self_harm_persons 0.51686092

opiates 0.41195709

marital_breakup 0.39971208

alone 0.31037882

self_reported_well_being 0.12949288

social_care_mh 0.20125278

homeless -0.32105739

alcohol_rx -0.07513134

drug_rx_opiate -0.14345307cor1 <- lm(suicide_rate ~ self_harm_persons, phe)

cor2 <- lm(suicide_rate ~ self_harm_persons + opiates, phe)

cor3 <- lm(suicide_rate ~ self_harm_persons + opiates + marital_breakup, phe)

cor4 <- lm(suicide_rate ~ self_harm_persons + opiates + marital_breakup +

children_leaving_care, phe)

cor5 <- lm(suicide_rate ~ self_harm_persons + opiates + marital_breakup +

children_leaving_care + depression, phe)

cor6 <- lm(suicide_rate ~ self_harm_persons + opiates + marital_breakup +

children_leaving_care + depression + homeless, phe)- Is the last model the best?

- Should we add more variables?

- Different variables?

9.7.1 Just “significant” variables?

Lets use any of the variables that had a p-value below 0.1.

# Changing model name method since now we will be looking at several models

sig1 <- lm(suicide_rate ~ children_leaving_care + self_harm_persons + opiates + marital_breakup + homeless, phe)

summary(sig1)

Call:

lm(formula = suicide_rate ~ children_leaving_care + self_harm_persons +

opiates + marital_breakup + homeless, data = phe)

Residuals:

Min 1Q Median 3Q Max

-3.8194 -1.1301 -0.1541 0.9383 5.6420

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 4.855937 1.449776 3.349 0.00104 **

children_leaving_care 0.037193 0.019703 1.888 0.06109 .

self_harm_persons 0.005501 0.002307 2.385 0.01840 *

opiates 0.123432 0.050315 2.453 0.01536 *

marital_breakup 0.218171 0.134664 1.620 0.10741

homeless -0.212926 0.075547 -2.818 0.00551 **

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 1.705 on 143 degrees of freedom

Multiple R-squared: 0.385, Adjusted R-squared: 0.3635

F-statistic: 17.91 on 5 and 143 DF, p-value: 9.201e-14autoplot(sig1)

Wait… now marital breakup isn’t significant?

# Changing model name method since now we will be looking at several models

sig2 <- lm(suicide_rate ~ children_leaving_care + self_harm_persons + opiates +

homeless, phe)

summary(sig2)

Call:

lm(formula = suicide_rate ~ children_leaving_care + self_harm_persons +

opiates + homeless, data = phe)

Residuals:

Min 1Q Median 3Q Max

-3.8777 -1.1053 0.0011 1.0022 5.8723

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 7.033367 0.546679 12.866 < 2e-16 ***

children_leaving_care 0.044142 0.019338 2.283 0.02392 *

self_harm_persons 0.006671 0.002203 3.028 0.00292 **

opiates 0.121234 0.050580 2.397 0.01782 *

homeless -0.227131 0.075459 -3.010 0.00309 **

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 1.714 on 144 degrees of freedom

Multiple R-squared: 0.3738, Adjusted R-squared: 0.3564

F-statistic: 21.49 on 4 and 144 DF, p-value: 6.473e-14autoplot(sig2)

- Relying on “statistical” significance means you will end-up shooting yourself in the foot, metaphorically speaking, i.e., make a bad model.

9.7.2 \(R^2\)? (Don’t use it to choose models).

Recall the definition of \(R^2\): It is the proportion of variability in the response variable explained by your predictor variables in the linear model.

Higher \(R^2\) is better, so maybe we should choose the model with the highest \(R^2\)?

- The full model has an \(R^2\) of 0.5031.

- After whittling down some variables due to multicollinearity,

model1has an \(R^2\) of 0.385. model2has an \(R^2\) of 0.3738.

So the full model is best! Right? All this stuff about variable elimination is pointless. I wasted hours of my life to get to this point…. No!

Never determine which is the best model via \(R^2\).

- \(R^2\) can be arbitrarily high when using many variables that may not be actually related to the response variable in any meaningful way.

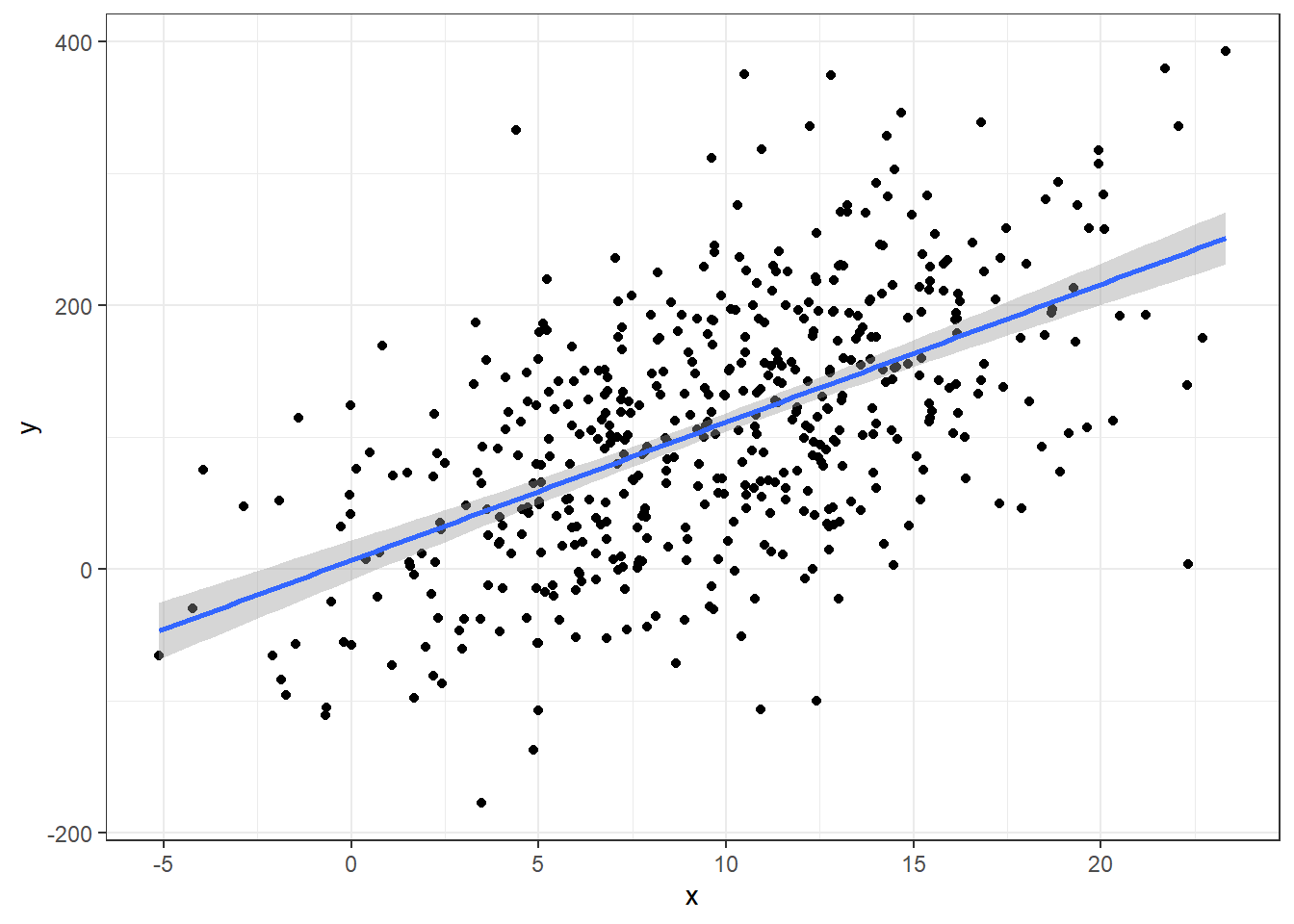

n = 500

a = 10; b = 10

### MAKING DATA WITH A TRUE LINEAR MODEL

x <- rnorm(n, 10, 5)

y = a + b*x + rnorm(n,0 ,80)

data <- data.frame(y,x)

ggplot(data, aes(x,y)) +

geom_point() +

geom_smooth(method = 'lm')

summary(lm(y ~ x, data))

Call:

lm(formula = y ~ x, data = data)

Residuals:

Min 1Q Median 3Q Max

-236.281 -55.592 -0.191 55.531 279.861

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 6.7071 7.6542 0.876 0.381

x 10.4567 0.6974 14.994 <2e-16 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 79.85 on 498 degrees of freedom

Multiple R-squared: 0.311, Adjusted R-squared: 0.3096

F-statistic: 224.8 on 1 and 498 DF, p-value: < 2.2e-16The R-squared here for the perfectly correct model is 0.3110227

- R-squared can be low even when you use the “correct” model.

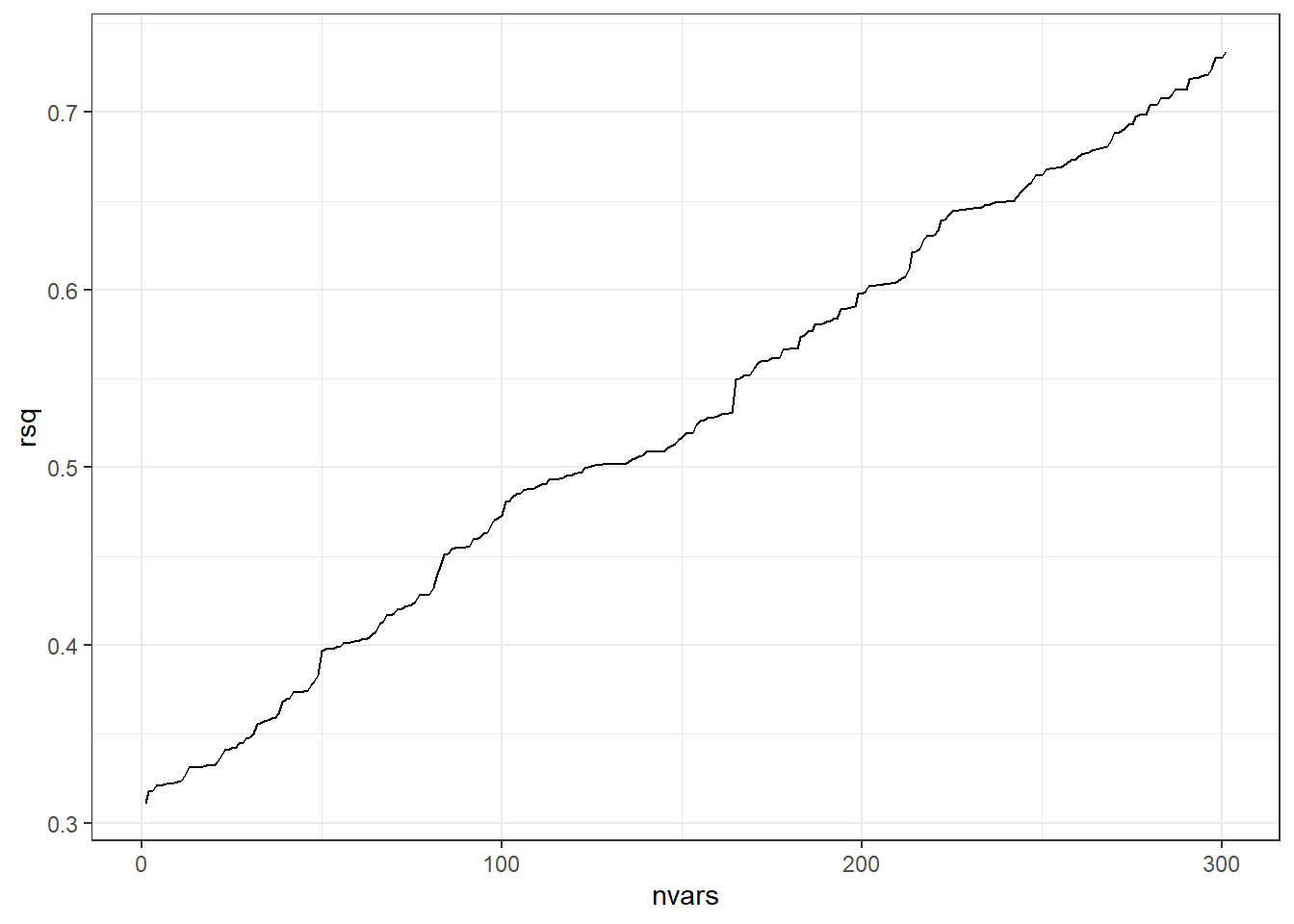

Now let’s throw in some irrelevant data and graph what happens to R-squared.

# Extra worthless predictors

p = 300

extra.predictors <- data.frame(matrix(rnorm(n*p), nrow=n))

full.data <- data.frame(data, extra.predictors)# need code to combine true and extra data

rsq = rep(NA, p+1)

for(iter in 1:(p+1)){

form <-formula(paste('y ~ ', paste(names(full.data)[2:(iter+1)], collapse=' + ')))

fit.mdl <- lm(form, data=full.data)

rsq[iter] <- summary(fit.mdl)$r.squared # Get the rsq value for the model.

}

ggplot(data.frame(nvars=1:(p+1), rsq),aes(x=nvars,y=rsq)) +

geom_path()

The beginning of the line on the left represents the R-squared value when using the one predictor variable that actually has any true relation with the response variable.

When we add on additional predictors (useless ones), R-squared always increases.

9.7.3 Adjusted \(R^2\) (More conservative)

\[R^2_{adj} = 1 - (1-R^2)\frac{n-1}{n-p-1}\] This is supposed to correct for the fact that \(R^2\) always increases with a greater number of variables (penalizes for the complexity of the model).

Here’s a table for most of the models we’ve discussed so far. It has both the adjusted and unadjusted form.

model Rsq AdjRsq

1 fullLm 0.5030783 0.3767423

2 redModel 0.4176079 0.3519246

3 cor1 0.2671452 0.2621598

4 cor2 0.3275478 0.3183361

5 cor3 0.3476621 0.3341654

6 cor4 0.3508866 0.3328556

7 cor5 0.3514271 0.3287497

8 cor6 0.3943409 0.3687496But… it doesn’t necessarily. Don’t trust it either.

9.7.4 Predicted \(R^2\) (Even more conservative)

Predicted R-squared or as I will write \(R^2{pred}\) is another play on the same idea as \(R^2\), except for it is based on taking out an observation, computing the regression model without it, then seeing how well the model predicts the left out value.

You can get it via the olsrr package using the ols_pred_rsq() function. The input is your model.

For instance, let us compare this to \(R^2\) from the performance package.

r2(fullLm)# R2 for Linear Regression

R2: 0.503

adj. R2: 0.377library(olsrr)

ols_pred_rsq(fullLm)[1] 0.1258262That’s a lot worse than the 0.503 for the unadjusted R-Squared

Here’s a new table including predicted R-squared

model Rsq AdjRsq PredRsq

1 fullLm 0.5030783 0.3767423 0.1258262

2 redModel 0.4176079 0.3519246 0.2264297

3 cor1 0.2671452 0.2621598 0.2445699

4 cor2 0.3275478 0.3183361 0.2929179

5 cor3 0.3476621 0.3341654 0.3003604

6 cor4 0.3508866 0.3328556 0.2948558

7 cor5 0.3514271 0.3287497 0.2818233

8 cor6 0.3943409 0.3687496 0.3218613- \(R^2\) only tells how well the model works on the data you have (overfitting kills its utility).

- \(R^2_{adj}\) tries to make an attempt at saying how well the model would work on the wider population/future observations.

- \(R^2_{pred}\) is probably the best measure of how well your model will actually work with new data.

- NONE of these are perfect so use these tools with caution and care.

9.7.5 Akaike Information Criterion AIC

One last point of discussion will be the Akaike Information Criterion.

\[AIC = 2(p+1) + n\log(SSE/n) - C\]

There’s a lot of theory behind this one and the Bayesian Information Criterion (BIC)

\[BIC = (p+1)\ln(n) + n\log(SSE/n) - C\]

This is where things get more confusing since AIC and BIC are numbers where SMALLER IS BETTER.

We will just be looking at AIC

model Rsq AdjRsq PredRsq AIC

1 fullLm 0.5030783 0.3767423 0.1258262 183.0882

2 redModel 0.4176079 0.3519246 0.2264297 176.7362

3 cor1 0.2671452 0.2621598 0.2445699 182.9770

4 cor2 0.3275478 0.3183361 0.2929179 172.1605

5 cor3 0.3476621 0.3341654 0.3003604 169.6356

6 cor4 0.3508866 0.3328556 0.2948558 170.8973

7 cor5 0.3514271 0.3287497 0.2818233 172.7732

8 cor6 0.3943409 0.3687496 0.3218613 164.5730Different measures will tell you different things.

Here \(R^2_{pred}\) and AIC agree that the cor6 model is the best.

cor6 <- lm(suicide_rate ~ self_harm_persons + opiates + marital_breakup +

children_leaving_care + depression + homeless, phe)So is that the one we use?

It’s not that simple.

9.8 Variable Selection Methods: Problems and Pitfalls

- Variable selection = methods for choosing which predictor variables to include in statistical models

- Focus on stepwise regression as a common but problematic approach

- Stepwise selection: automated process of adding/removing variables based on statistical significance (p-values and model fit)

9.8.1 Major Problems with Stepwise Selection

9.8.1.1 1. Biased R-squared Values

- R-squared values are inflated

- Makes model appear to explain more variation than it actually does

- Gives false confidence in model’s predictive ability

9.8.1.2 2. Invalid Statistical Inference

- P-values are too small (not valid)

- Confidence intervals are too narrow

- Doesn’t account for multiple testing problem

- Standard errors are biased low

9.8.1.3 3. Biased Regression Coefficients

- Coefficients are biased away from zero

- More likely to select variables with overestimated effects

- Selection process favors chance findings

- True effects may be much smaller than estimated

9.8.1.4 4. Model Instability

- Results highly dependent on sample

- Small changes in data can lead to different variables being selected

- Poor reproducibility

- Different samples likely to produce different models

9.8.2 Example: House Price Prediction

- Scenario: 20 potential predictors of house prices

- First sample might select:

- Square footage

- Number of bathrooms

- Lot size

- Second sample might select completely different variables:

- Age of house

- Number of bedrooms

- Distance to downtown

- Demonstrates instability of selection process

9.8.3 Better Alternatives

9.8.3.1 1. Theory-Driven Selection

- Use subject matter knowledge

- Select variables based on theoretical importance

- Include known important predictors regardless of significance

9.8.3.2 2. Include More Variables

- Keep theoretically important variables

- Don’t eliminate based solely on statistical significance

- Better to include too many than too few important variables

- Degrees of freedom permitting of course!

9.8.3.3 3. Alternative Dimension Reduction Methods

- Principal Components Analysis

- Regularization methods (LASSO, Ridge regression)

- Data reduction techniques that don’t use outcome variable

9.8.4 Key Takeaways

- Avoid automated variable selection methods

- Don’t let computational convenience override good statistical practice

- Complex but theoretically sound models preferred over overly simplified ones

- Statistical significance shouldn’t be the sole criterion for variable inclusion

10 Prespecification of Predictor Complexity in Statistical Modeling

10.1 I. Introduction to Linear Relationships

- Truly linear relationships are rare in real-world data

- Notable exception: Same measurements at different timepoints

- Example: Blood pressure before and after treatment

- Most relationships between predictors and outcomes are nonlinear

- Linear modeling often chosen due to data limitations, not reality

10.2 Problems with Post-Hoc Simplification

10.2.1 Common but Problematic Approaches:

- Examining scatter plots

- Checking descriptive statistics

- Using informal assessments

- Modifying model based on these observations

10.2.2 Key Issue:

- Creates “phantom degrees of freedom”

- Informal assessments use degrees of freedom not accounted for in:

- Standard errors

- P-values

- R² values

10.3 The Prespecification Approach

10.3.1 Core Principles:

- Decide on predictor complexity before examining relationships

- Base decisions on:

- Effective sample size

- Prior knowledge

- Expected predictor importance

- Maintain decisions regardless of analysis results

10.3.2 Benefits:

- More reliable statistical inference

- Better representation of uncertainty

- Prevention of bias from data-driven simplification

10.4 Practical Implementation

10.4.1 Guidelines for Complexity:

- Allow more complex representations for:

- Stronger expected relationships

- Larger effective sample sizes

- More important predictors

10.4.2 Examples of Implementation:

- Using splines with more knots for important predictors

- Scaling complexity to sample size

- Matching complexity to theoretical importance

10.5 Validation and Testing

10.5.1 Allowed Practices:

- Graphing estimated relationships

- Performing nonlinearity tests

- Presenting results to readers

10.5.2 Important Rule:

- Maintain prespecified complexity even if simpler relationships appear adequate

10.6 The Directional Principle

10.6.1 Key Concepts:

- Moving simple → complex

- Degrees of freedom properly increase

- Statistical tests maintain distribution

- Moving complex → simple

- Requires special adjustments

- May compromise statistical validity

10.7 Importance and Impact

10.7.1 Benefits of Prespecification:

- Prevents optimistic performance estimates

- Maintains valid statistical inference

- Provides reliable predictions

- Avoids data-driven simplification bias

10.7.2 Trade-offs:

- May appear conservative

- Slight overfitting preferred to spurious precision

10.8 Summary

- Prespecify predictor complexity based on prior knowledge

- Avoid data-driven simplification

- Maintain statistical validity through consistent approach

- Better to slightly overfit than create spuriously precise estimates

10.9 Sample Size Requirements & Overfitting in Regression Models

10.9.1 Definition

- Overfitting occurs when model complexity exceeds data information content

- Results in:

- Inflated measures of model performance (e.g., R²)

- Poor prediction on new data

- Model fits noise rather than signal

10.9.1.1 Visual Example

Consider two models of the same data:

Simple model: y ~ x

Overfit model: y ~ x + x² + x³ + x⁴ + ...10.9.2 The m/15 Rule

10.9.2.1 Limiting Sample Size (m)

| Type of Response | Limiting Sample Size (m) |

|---|---|

| Continuous | Total sample size (n) |

| Binary | min(n₁, n₂) smaller group |

| Ordinal (k categories) | n - (1/n)Σnᵢ³ |

| Survival time | Number of events/failures |

10.9.2.2 Basic Rule

- Number of parameters (p) should be < m/15

- Some situations require more conservative p < m/20

- Less conservative p < m/10 possible

10.9.3 Counting Parameters

10.9.3.1 Include ALL of these in your count:

- Main predictor variables

- Nonlinear terms

- Interaction terms

- Dummy variables for categorical predictors (k-1)

10.9.3.2 Example Parameter Count

Model components:

- Age (nonlinear, 3 knots) = 2 parameters

- Sex (binary) = 1 parameter

- Treatment (3 categories) = 2 parameters

- Age × Treatment interaction = 4 parameters

Total = 9 parameters10.9.4 Special Considerations

10.9.4.1 Need More Conservative Ratios When:

- Predictors have narrow distributions

- e.g., age range 30-45 years only

- Highly unbalanced categorical variables

- e.g., 95% in one category

- Clustered measurements

- Small effect sizes expected

10.9.5 Practical Example

10.9.5.1 Binary Outcome Study

Study population:

- 1000 total patients

- 100 heart attacks

- 900 no heart attacks

Calculations:

m = min(100, 900) = 100

Maximum parameters = 100/15 ≈ 6-710.9.6 Alternative Approaches

10.9.6.1 Other Methods to Assess/Prevent Overfitting:

- Shrinkage estimates

- Cross-validation

- Bootstrap validation

- Penalized regression methods

10.9.7 Sample Size for Variance Estimation

- Need ~70 observations for ±20% precision in \(\sigma\) estimate

- Affects all standard errors and p-values

- Critical for reliable inference

10.9.8 Key Takeaways

- Count Everything: Include all terms in parameter count

- Be Conservative: Use m/15 as starting point

- Consider Context: Adjust for data peculiarities

- Validate: Use shrinkage or cross-validation

- Simplify: Prefer simpler models when in doubt

10.9.9 Practice Problems

Calculate maximum parameters for:

- 500 patients, continuous outcome

- 1000 patients, 150 events (survival)

- 300 patients, 50/250 binary outcome

Count parameters in model:

y ~ age + age² + sex + treatment*race where treatment has 3 levels and race has 4 levels

10.10 Shrinkage in Statistical Models: Understanding the Basics

10.10.1 Introduction

- Statistical models can suffer from overfitting

- Overfitting: model performs well on training data but poorly on new data

- Similar to memorizing test answers without understanding concepts

- Need methods to make models more reliable and generalizable

10.10.2 What is Shrinkage?

- Technique to prevent overfitting

- Makes model predictions more conservative and reliable

- Acts like a “leash” on model coefficients

- Helps handle regression to the mean

10.10.3 Example

- Study of 10 different medical treatments

- Some treatments appear very effective by chance

- When tested on new patients, effects usually less extreme

- Natural tendency for extreme results to move toward average

- This movement toward average is “shrinkage”

10.10.4 Key Shrinkage Methods

10.10.4.1 1. Ridge Regression

- Adds penalty to prevent large coefficients

- Characteristics:

- Like rubber band pulling coefficients toward zero

- Keeps all variables in model

- Reduces size of effects

- Ideal for correlated predictors

10.10.4.2 2. LASSO Regression

- Least Absolute Shrinkage and Selection Operator

- Characteristics:

- Can force coefficients to exactly zero

- Performs variable selection

- Creates simpler models

- Good for identifying important variables

10.10.5 Benefits of Shrinkage

- More stable predictions

- Better performance on new data

- Protection against overfitting

- More reliable assessment of variable importance

10.10.6 Key Takeaway

- Shrinkage represents statistical humility

- Prevents extreme predictions based on limited data

- Makes models more reliable and practical

10.11 Data Reduction Methods

10.11.1 Definition

- Process of reducing number of parameters in statistical models

- Focus on dimension reduction without using response variable Y

- “Unsupervised” approach to prevent overfitting

10.11.2 Purpose

- Improve model stability

- Reduce overfitting

- Maintain statistical inference validity

- Handle situations with many predictors relative to sample size

10.11.3 Redundancy Analysis

- Core Concept

- Identifies predictors well-predicted by other predictors

- Removes redundant variables systematically

- Implementation Process

- Convert predictors to appropriate forms

- Continuous → restricted cubic splines

- Categorical → dummy variables

- Use OLS for prediction

- Remove highest R² predictors

- Iterate until threshold reached

- Convert predictors to appropriate forms

10.11.4 Variable Clustering

- Purpose

- Group related predictors

- Identify independent dimensions

- Simplify model structure

- Methods

- Statistical clustering with correlations

- Principal component analysis (oblique rotation)

- Hierarchical cluster analysis

- Important Considerations

- Use robust measures for skewed variables

- Consider rank-based measures

- Hoeffding’s D for non-monotonic relationships

10.11.5 Variable Transformation and Scaling

- Key Methods

- Maximum Total Variance (MTV)

- Maximum Generalized Variance (MGV)

- Process Goals

- Optimize variable transformations

- Maximize relationships between predictors

- Reduce complexity

- Benefits

- Fewer nonlinear terms needed

- Better interpretability

- More meaningful combinations

10.11.6 Simple Scoring of Variable Clusters

- Approaches

- First principal component

- Weighted sums

- Expert-assigned severity points

- Common Applications

- Binary predictor groups

- Hierarchical scoring systems

- Implementation-focused solutions

10.12 Implementation Guidelines

10.12.1 Best Practices

- Prioritize subject matter knowledge

- Validate without response variable

- Use independent data for validation

- Document reduction decisions

- Balance simplicity vs. information

10.12.2 Recommended Workflow

- Start with redundancy analysis

- Apply variable clustering

- Transform within clusters if needed

- Create simple scores where appropriate

- Validate each step

10.13 Key Considerations

10.13.1 Advantages

- Prevents overfitting

- Maintains statistical validity

- Improves model stability

- Enhances interpretability

10.13.2 Limitations

- Potential information loss

- Trade-off with complexity

- Need for validation

10.14 Discussion Points

10.14.1 Critical Questions

- Choosing between methods

- Determining optimal clusters

- Balancing complexity and interpretability

10.14.2 Implementation Challenges

- Deciding on thresholds

- Handling mixed variable types

- Validating reduction decisions

10.14.3 Remarks

- Essential for stable modeling with many predictors

- Requires thoughtful method combination

- Focus on maintaining predictive power

- Ensure statistical validity

10.15 Data Reduction Techniques Examples

First, let’s load the required packages and prepare our data:

library(Hmisc)

library(rms)

library(pcaPP)

# Read the data

df <- read.csv(here::here(

"datasets",

"phe.csv"))- We have 149 rows of data

- We want to investigate the continuous outcome of

suicide_rate - m/15 rule: we can only have about 10 parameters in the model (we could be more liberal in loosen it to 15 variables)

10.15.1 1. Redundancy Analysis

Redundancy analysis helps identify predictors that can be well-predicted from other variables:

# Perform redundancy analysis

df2 = df %>% dplyr::select(-suicide_rate)

redun_result <- redun(~ .,

data=df, r2=0.6)

# Print results

redun_result

Redundancy Analysis

~.

n: 149 p: 31 nk: 3

Number of NAs: 0

Transformation of target variables forced to be linear

R-squared cutoff: 0.6 Type: ordinary

R^2 with which each variable can be predicted from all other variables:

children_youth_justice adult_carers_isolated_18

0.474 0.634

adult_carers_isolated_all_ages adult_carers_not_isolated

0.612 0.769

alcohol_rx_18 alcohol_rx_all_ages

0.965 0.998

alcohol_admissions_f alchol_admissions_m

0.999 1.000

alcohol_admissions_p children_leaving_care

0.686 0.832

depression domestic_abuse

0.738 0.729

self_harm_female self_harm_male

1.000 1.000

self_harm_persons opiates

1.000 0.952

lt_health_problems lt_unepmloyment

0.945 0.876

looked_after_children marital_breakup

0.889 0.706

old_pople_alone alone

0.956 0.906

self_reported_well_being smi

0.520 0.859

social_care_mh homeless

0.513 0.790

alcohol_rx drug_rx_non_opiate

0.761 0.787

drug_rx_opiate suicide_rate

0.658 0.639

unemployment

0.926

Rendundant variables:

self_harm_persons alchol_admissions_m alcohol_rx_all_ages alcohol_rx_18

old_pople_alone self_harm_male unemployment looked_after_children

lt_health_problems smi drug_rx_non_opiate opiates children_leaving_care

alcohol_admissions_f homeless self_harm_female

Predicted from variables:

children_youth_justice adult_carers_isolated_18

adult_carers_isolated_all_ages adult_carers_not_isolated

alcohol_admissions_p depression domestic_abuse lt_unepmloyment

marital_breakup alone self_reported_well_being social_care_mh

alcohol_rx drug_rx_opiate suicide_rate

Variable Deleted R^2

1 self_harm_persons 1.000

2 alchol_admissions_m 1.000

3 alcohol_rx_all_ages 0.978

4 alcohol_rx_18 0.960

5 old_pople_alone 0.950

6 self_harm_male 0.927

7 unemployment 0.896

8 looked_after_children 0.866

9 lt_health_problems 0.802

10 smi 0.783

11 drug_rx_non_opiate 0.727

12 opiates 0.718

13 children_leaving_care 0.704

14 alcohol_admissions_f 0.684

15 homeless 0.663

16 self_harm_female 0.600

R^2 after later deletions

1 1 1 1 1 0.987 0.987 0.986 0.986 0.986 0.985 0.985 0.984 0.981 0.981 0.625

2 0.997 0.997 0.997 0.996 0.996 0.996 0.996 0.996 0.996 0.996 0.996 0.7 0.696 0.665

3 0.978 0.978 0.977 0.977 0.976 0.974 0.973 0.972 0.972 0.972 0.717 0.713 0.677

4 0.959 0.955 0.952 0.951 0.951 0.947 0.947 0.792 0.787 0.755 0.751 0.742

5 0.949 0.941 0.941 0.83 0.809 0.801 0.765 0.765 0.753 0.731 0.722

6 0.925 0.923 0.921 0.92 0.917 0.915 0.912 0.895 0.891 0.636

7 0.892 0.888 0.883 0.883 0.878 0.867 0.856 0.85 0.848

8 0.862 0.86 0.859 0.853 0.777 0.755 0.751 0.722

9 0.794 0.792 0.783 0.782 0.768 0.753 0.733

10 0.781 0.746 0.741 0.724 0.713 0.704

11 0.724 0.718 0.717 0.716 0.702

12 0.712 0.691 0.689 0.673

13 0.689 0.674 0.637

14 0.681 0.656

15 0.657

16 As with our section on multicollinarity, we can see that a number of variables are redundant. If we were to remove all these variables we would at least satisfy m/10 which is a bit more liberal than the m/15 guidance.

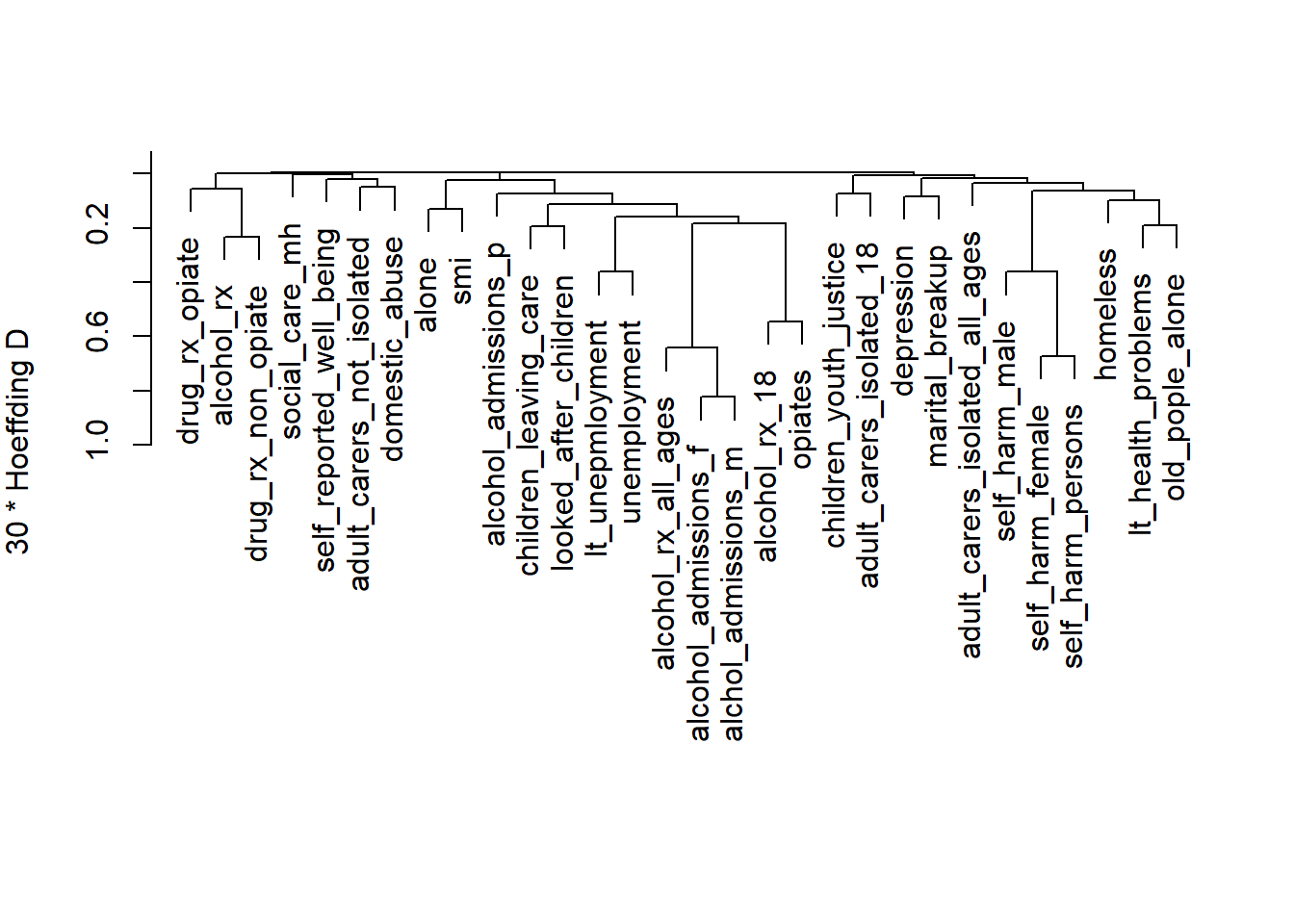

10.15.2 2. Variable Clustering

Let’s perform hierarchical clustering on our variables to identify related groups:

# Perform variable clustering

vc <- varclus(~ .,

data=df2, sim= 'hoeffding')

# Plot dendrogram

plot(vc)

- We can see a lot of the variables clustering together

10.15.3 3. Principal Components Analysis

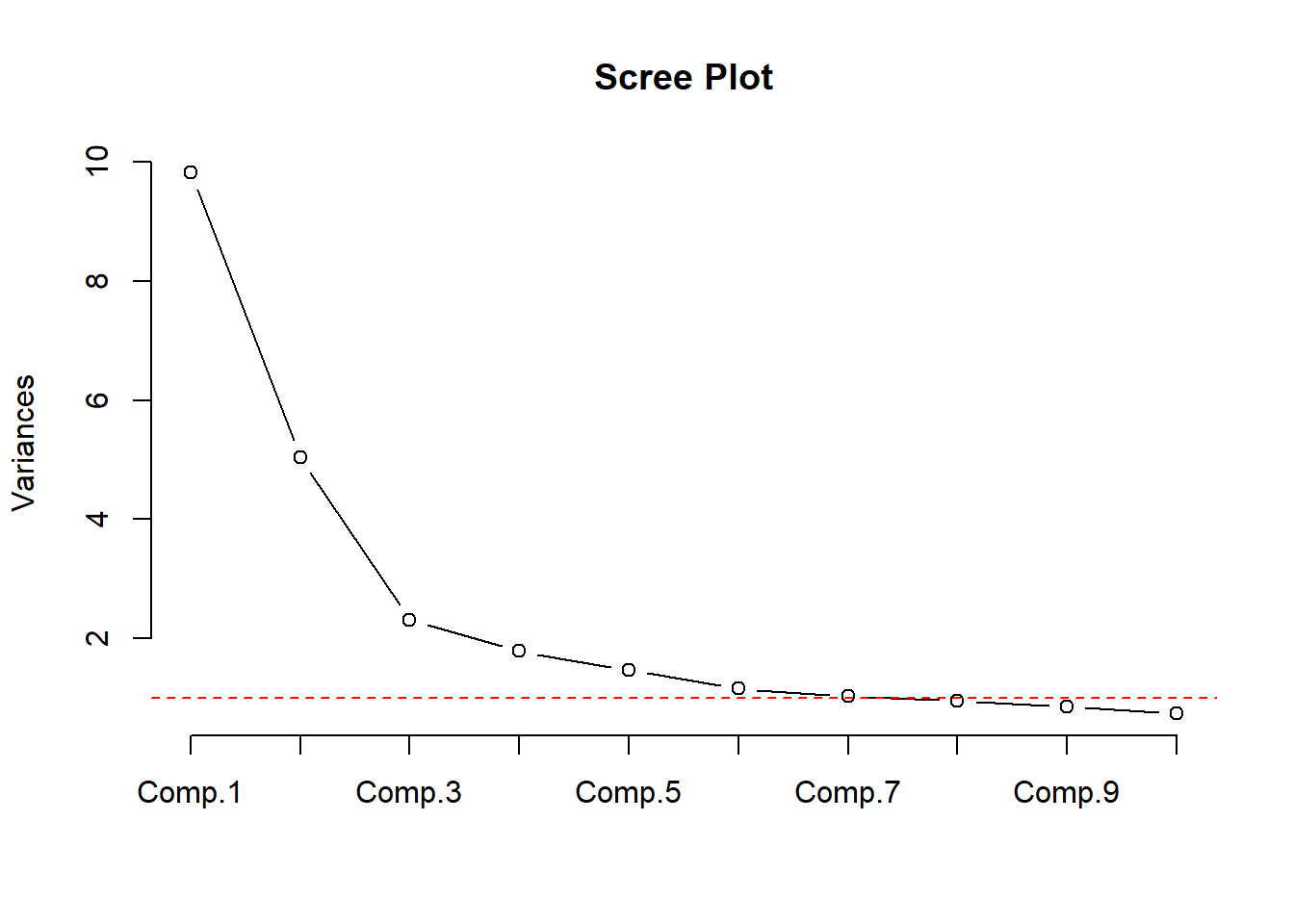

Let’s examine the data structure using PCA:

# Perform PCA

pca_result <- princomp(df2, cor=TRUE)

# Scree plot

plot(pca_result, type="lines", main="Scree Plot")

abline(h=1, lty=2, col="red") # Kaiser criterion line

# Print variance explained by first few components

summary(pca_result, loadings=TRUE, cutoff=0.3)Importance of components:

Comp.1 Comp.2 Comp.3 Comp.4 Comp.5

Standard deviation 3.1327307 2.2436841 1.51857984 1.33713169 1.21224371

Proportion of Variance 0.3271334 0.1678039 0.07686949 0.05959737 0.04898449

Cumulative Proportion 0.3271334 0.4949373 0.57180682 0.63140419 0.68038869

Comp.6 Comp.7 Comp.8 Comp.9 Comp.10

Standard deviation 1.07625280 1.01836888 0.9747646 0.92320127 0.86023787

Proportion of Variance 0.03861067 0.03456917 0.0316722 0.02841002 0.02466697

Cumulative Proportion 0.71899936 0.75356853 0.7852407 0.81365075 0.83831772

Comp.11 Comp.12 Comp.13 Comp.14 Comp.15

Standard deviation 0.76164102 0.74326524 0.70575177 0.67895928 0.65072428

Proportion of Variance 0.01933657 0.01841477 0.01660285 0.01536619 0.01411474

Cumulative Proportion 0.85765429 0.87606907 0.89267192 0.90803811 0.92215284

Comp.16 Comp.17 Comp.18 Comp.19 Comp.20

Standard deviation 0.62502778 0.57314172 0.56636534 0.55357002 0.478567350

Proportion of Variance 0.01302199 0.01094971 0.01069232 0.01021466 0.007634224

Cumulative Proportion 0.93517484 0.94612455 0.95681687 0.96703153 0.974665755

Comp.21 Comp.22 Comp.23 Comp.24

Standard deviation 0.473155304 0.413788556 0.340046283 0.302671397

Proportion of Variance 0.007462531 0.005707366 0.003854382 0.003053666

Cumulative Proportion 0.982128287 0.987835652 0.991690035 0.994743701

Comp.25 Comp.26 Comp.27 Comp.28

Standard deviation 0.250796490 0.224198463 0.174227171 0.1176538993

Proportion of Variance 0.002096629 0.001675498 0.001011837 0.0004614147

Cumulative Proportion 0.996840330 0.998515828 0.999527665 0.9999890799

Comp.29 Comp.30

Standard deviation 1.669952e-02 6.980650e-03

Proportion of Variance 9.295803e-06 1.624316e-06

Cumulative Proportion 9.999984e-01 1.000000e+00

Loadings:

Comp.1 Comp.2 Comp.3 Comp.4 Comp.5 Comp.6 Comp.7

children_youth_justice 0.378 0.580

adult_carers_isolated_18 0.413 0.307

adult_carers_isolated_all_ages

adult_carers_not_isolated

alcohol_rx_18

alcohol_rx_all_ages

alcohol_admissions_f

alchol_admissions_m

alcohol_admissions_p

children_leaving_care

depression

domestic_abuse 0.342

self_harm_female

self_harm_male

self_harm_persons

opiates

lt_health_problems

lt_unepmloyment

looked_after_children

marital_breakup

old_pople_alone 0.338

alone -0.434

self_reported_well_being 0.381

smi -0.366

social_care_mh 0.488

homeless -0.325

alcohol_rx -0.543

drug_rx_non_opiate -0.558

drug_rx_opiate -0.397

unemployment

Comp.8 Comp.9 Comp.10 Comp.11 Comp.12 Comp.13

children_youth_justice

adult_carers_isolated_18

adult_carers_isolated_all_ages 0.351 -0.499 -0.301

adult_carers_not_isolated

alcohol_rx_18

alcohol_rx_all_ages

alcohol_admissions_f

alchol_admissions_m

alcohol_admissions_p -0.378

children_leaving_care

depression 0.340 0.373

domestic_abuse -0.397 0.304

self_harm_female

self_harm_male

self_harm_persons

opiates 0.335

lt_health_problems

lt_unepmloyment

looked_after_children

marital_breakup -0.316 -0.366 0.442

old_pople_alone -0.344

alone

self_reported_well_being 0.605 -0.374

smi

social_care_mh -0.618

homeless

alcohol_rx

drug_rx_non_opiate

drug_rx_opiate 0.312 -0.320

unemployment

Comp.14 Comp.15 Comp.16 Comp.17 Comp.18 Comp.19

children_youth_justice 0.376

adult_carers_isolated_18 -0.505 -0.378

adult_carers_isolated_all_ages 0.304

adult_carers_not_isolated -0.390 0.510 -0.459

alcohol_rx_18

alcohol_rx_all_ages

alcohol_admissions_f

alchol_admissions_m

alcohol_admissions_p 0.376 -0.366

children_leaving_care 0.393

depression -0.304 0.406 -0.387

domestic_abuse 0.311

self_harm_female

self_harm_male

self_harm_persons

opiates -0.305

lt_health_problems

lt_unepmloyment -0.448 -0.334

looked_after_children

marital_breakup

old_pople_alone

alone

self_reported_well_being

smi

social_care_mh

homeless 0.483

alcohol_rx

drug_rx_non_opiate 0.338

drug_rx_opiate -0.382

unemployment

Comp.20 Comp.21 Comp.22 Comp.23 Comp.24 Comp.25

children_youth_justice

adult_carers_isolated_18

adult_carers_isolated_all_ages

adult_carers_not_isolated

alcohol_rx_18

alcohol_rx_all_ages

alcohol_admissions_f

alchol_admissions_m

alcohol_admissions_p

children_leaving_care -0.469

depression

domestic_abuse

self_harm_female 0.495

self_harm_male -0.668

self_harm_persons

opiates

lt_health_problems 0.423

lt_unepmloyment 0.422

looked_after_children 0.634 0.429

marital_breakup -0.370

old_pople_alone 0.307

alone -0.441

self_reported_well_being

smi 0.561 -0.314

social_care_mh

homeless 0.349

alcohol_rx 0.525

drug_rx_non_opiate -0.316 -0.454

drug_rx_opiate

unemployment -0.659

Comp.26 Comp.27 Comp.28 Comp.29 Comp.30

children_youth_justice

adult_carers_isolated_18

adult_carers_isolated_all_ages

adult_carers_not_isolated

alcohol_rx_18 0.342 -0.625

alcohol_rx_all_ages -0.760

alcohol_admissions_f 0.590 0.513

alchol_admissions_m -0.806

alcohol_admissions_p

children_leaving_care

depression

domestic_abuse

self_harm_female 0.487

self_harm_male -0.353 0.338

self_harm_persons -0.804

opiates -0.379 0.435

lt_health_problems 0.479

lt_unepmloyment

looked_after_children

marital_breakup

old_pople_alone -0.488

alone

self_reported_well_being

smi

social_care_mh

homeless

alcohol_rx

drug_rx_non_opiate

drug_rx_opiate

unemployment -0.312 10.15.4 4. Sparse Principal Components Analysis

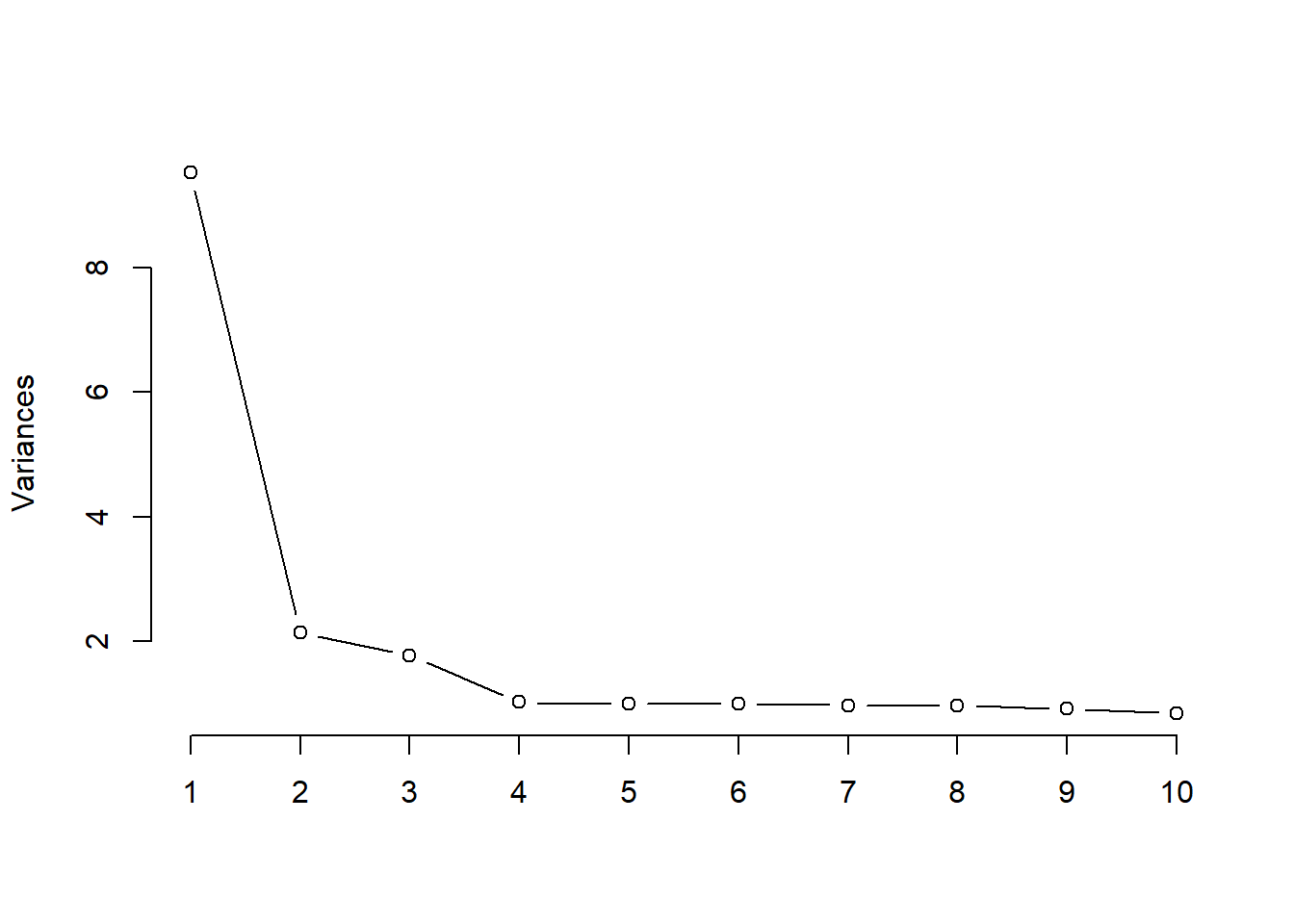

Using pcaPP for robust sparse PCA.

# Perform sparse PCA

sparse_pca <- sPCAgrid(df2, k=10, method = 'sd' ,

center =mean , scale =sd , scores =TRUE ,

maxiter =10)

# Plot variance explained

plot(sparse_pca,type = 'lines' , main= ' ')

# Print loadings

print(sparse_pca$loadings)

Loadings:

Comp.1 Comp.2 Comp.3 Comp.4 Comp.5 Comp.6 Comp.7

children_youth_justice 1.000

adult_carers_isolated_18

adult_carers_isolated_all_ages 0.464

adult_carers_not_isolated 0.252

alcohol_rx_18 0.295

alcohol_rx_all_ages 0.305

alcohol_admissions_f 0.295

alchol_admissions_m 0.303

alcohol_admissions_p 0.161

children_leaving_care 0.248

depression 0.111

domestic_abuse 0.106 0.791

self_harm_female 0.131 -0.264

self_harm_male 0.222

self_harm_persons 0.176

opiates 0.278

lt_health_problems 0.210

lt_unepmloyment 0.226

looked_after_children 0.300

marital_breakup 0.113

old_pople_alone 0.636

alone 0.122 -0.607

self_reported_well_being 0.965

smi 0.122

social_care_mh 1.000

homeless -0.613

alcohol_rx 0.707

drug_rx_non_opiate 0.707

drug_rx_opiate

unemployment 0.234

Comp.8 Comp.9 Comp.10

children_youth_justice

adult_carers_isolated_18

adult_carers_isolated_all_ages

adult_carers_not_isolated

alcohol_rx_18

alcohol_rx_all_ages

alcohol_admissions_f

alchol_admissions_m

alcohol_admissions_p -0.574

children_leaving_care

depression 0.903

domestic_abuse

self_harm_female

self_harm_male

self_harm_persons 0.444

opiates

lt_health_problems

lt_unepmloyment

looked_after_children

marital_breakup 0.819

old_pople_alone

alone

self_reported_well_being

smi

social_care_mh

homeless

alcohol_rx

drug_rx_non_opiate

drug_rx_opiate 0.896

unemployment -0.426

Comp.1 Comp.2 Comp.3 Comp.4 Comp.5 Comp.6 Comp.7 Comp.8 Comp.9

SS loadings 1.000 1.000 1.000 1.000 1.000 1.000 1.000 1.000 1.000

Proportion Var 0.033 0.033 0.033 0.033 0.033 0.033 0.033 0.033 0.033

Cumulative Var 0.033 0.067 0.100 0.133 0.167 0.200 0.233 0.267 0.300

Comp.10

SS loadings 1.000

Proportion Var 0.033

Cumulative Var 0.333Like are variable clutstering, we can see that lots of variables load onto the first principal component. We could add component 1 to our regression model and keep the rest of the variables (not those loaded on comp. 1).

However, let’s instead use stepwise regression only on the preditors in combination with sparse PCA to select variables for 10 components in our model.

- Stepwise here tells us which predictors that load onto each PC are needed to predict that pc

spca1 <- princmp(df2, sw = TRUE ,

k = 10,

kapprox = 10,

method = "sparse",

cor = TRUE,

nvmax = 30)

print(spca1)Sparse Principal Components Analysis

Stepwise Approximations to PCs With Cumulative R^2

PC 1

alchol_admissions_m (0.975) + self_harm_persons (0.999) +

looked_after_children (1)

PC 2

adult_carers_isolated_all_ages (0.759) + homeless (0.978) +

old_pople_alone (1)

PC 3

drug_rx_non_opiate (0.89) + alcohol_rx (1)

PC 4

self_harm_female (1)

PC 5

adult_carers_isolated_18 (0.861) + self_harm_female (1)

PC 6

self_harm_female (0.993) + self_reported_well_being (1)

PC 7

social_care_mh (1)

PC 8

children_youth_justice (1)

PC 9

domestic_abuse (0.872) + alone (1)

PC 10

depression (0.875) + unemployment (0.999) + old_pople_alone (1)We get 10 components, some with many predictors, some with only one.

10.15.5 Put it all together

Using theory, we could decide to create cluster scores for some of these components, while others with only 2 variables we might want to just eliminate one of the variables.

For those that we want to have a composite score, we can use the first principal component of their scores. Or, if we want to use this scoring outside of this context we can get a regression model on the first PC.

Let me demonstrate with our first component from the sparse PCA.

# Get pc scores for the first sparse PC variables

pc1_scores = princmp(df2[,c(names(spca1$sw[[1]]))],

method = "regular",

cor = TRUE)$scores[,1]

df2$pc1_scores = pc1_scores

mod1 = lm(pc1_scores~alchol_admissions_m + self_harm_persons , data = df2)

parameters::parameters(mod1) |> print_md()| Parameter | Coefficient | SE | 95% CI | t(146) | p |

|---|---|---|---|---|---|

| (Intercept) | -6.53 | 0.18 | (-6.88, -6.17) | -36.38 | < .001 |

| alchol admissions m | 3.63e-03 | 1.47e-04 | (3.34e-03, 3.92e-03) | 24.70 | < .001 |

| self harm persons | 9.09e-03 | 4.38e-04 | (8.22e-03, 9.95e-03) | 20.75 | < .001 |

Now, we could report those regression coefficients to get a pretty reasonable estimate of the scoring for that component of the model.

Now, let’s get the second and third scores as well.

# Get pc scores for the second sparse PC variables

pc2_scores = princmp(df2[,c(names(spca1$sw[[2]]))],

method = "regular",

cor = TRUE)$scores[,1]

df2$pc2_scores = pc2_scores

pc3_scores = princmp(df2[,c(names(spca1$sw[[3]]))],

method = "regular",

cor = TRUE)$scores[,1]

df2$pc3_scores = pc3_scoresFor the rest, we will simplify things a bit and just use the first variable of the remaining 10 sparse PCA components.

Let’s now fit a model based using our 3 PCs and the 7 other variables we selected.

df_all = df2 %>%

select(pc1_scores, pc2_scores, pc3_scores,

self_harm_female,

adult_carers_isolated_18,

self_harm_female,

social_care_mh,

children_youth_justice,

domestic_abuse,

depression)

df_all$suicide_rate = df$suicide_rate

# 10 predictors, 1 outcome, 149 observations

model_all = lm(

data = df_all,

suicide_rate ~ .

)

summary(model_all)

Call:

lm(formula = suicide_rate ~ ., data = df_all)

Residuals:

Min 1Q Median 3Q Max

-4.2067 -1.1131 -0.1051 0.9371 4.1430

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 9.6296409 1.6223906 5.935 2.22e-08 ***

pc1_scores 0.5747571 0.1555263 3.696 0.000315 ***

pc2_scores 0.3436984 0.1388871 2.475 0.014539 *

pc3_scores -0.1009508 0.1084578 -0.931 0.353579

self_harm_female 0.0025597 0.0024544 1.043 0.298819

adult_carers_isolated_18 0.0239721 0.0243409 0.985 0.326408

social_care_mh 0.0010556 0.0004836 2.183 0.030729 *

children_youth_justice -0.0310969 0.0241586 -1.287 0.200165

domestic_abuse 0.0266173 0.0359734 0.740 0.460599

depression -0.1202582 0.1114831 -1.079 0.282584

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 1.729 on 139 degrees of freedom

Multiple R-squared: 0.3853, Adjusted R-squared: 0.3455

F-statistic: 9.681 on 9 and 139 DF, p-value: 2.122e-11Now let’s check our assumptions:

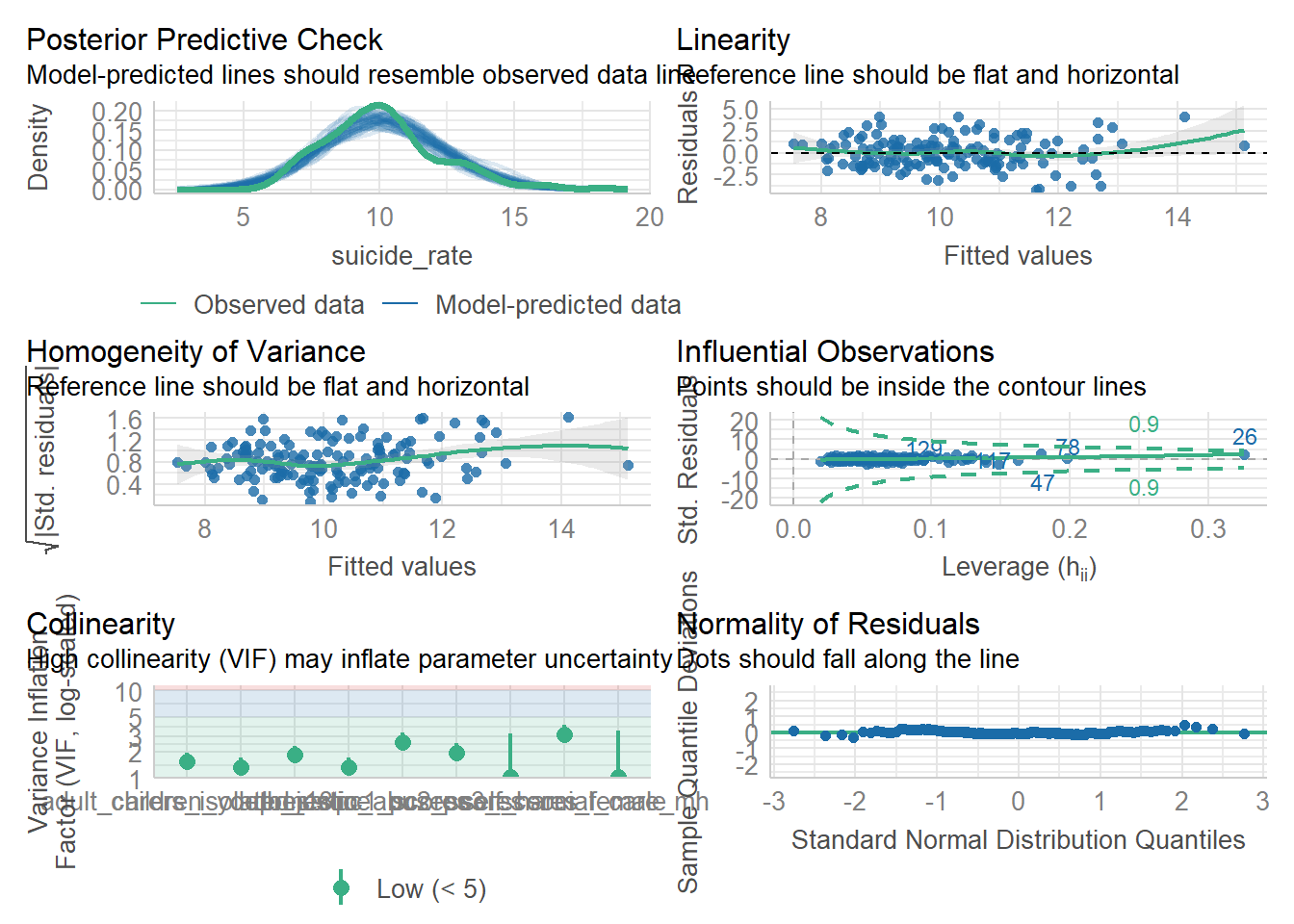

check_model(model_all)

10.15.6 Analysis Summary

From the redundancy analysis, we can identify variables that are highly predictable from others, helping reduce dimensionality while maintaining information.

The variable clustering dendrogram shows natural groupings in our data, which can guide feature selection or creation of composite scores.

The PCA results show how many components are needed to explain a certain percentage of variance in the data.

Sparse PCA provides a more interpretable solution by forcing some loadings to zero while maintaining most of the explained variance.

10.15.7 Recommendations for Data Reduction

Based on these analyses, we can recommend:

Consider combining highly correlated variables within the same cluster into composite scores

Use the first few principal components if dimension reduction is needed while maintaining maximum variance

For interpretability, consider using the sparse PCA solution which provides clearer variable groupings

Remove redundant variables identified in the redundancy analysis on an as needed basis. Justify your choices!

These techniques provide different perspectives on data reduction, and the choice depends on the specific needs of the analysis (interpretability, variance preservation, or prediction accuracy).